Archive for the ‘HealthCare IT’ Category

Protected: KOL on Competitive Dynamics: LPBI Group’s Founder’s Radar Screens on AI in Health, Life Sciences & BioPharma

Posted in Artificial Intelligence - Breakthroughs in Theories and Technologies, Artificial Intelligence - General, Artificial Intelligence Applications in Health Care, Artificial Intelligence in Medicine - Application for Diagnosis, Artificial Intelligence in Medicine - Applications in Therapeutics, BioTechnology - Venture Creation, BioTechnology - Venture Creation, Venture Capital, Disease Biology, Small Molecules in Development of Therapeutic Drugs, Drug Delivery Platform Technology, Drug Development Process, Drug Discovery Chemistry, drug repurposing, Genetics & Pharmaceutical, Global Market of Medical Devices Technology, Global Partnering & Biotech Investment, HealthCare IT, Personalized and Precision Medicine & Genomic Research, Pharmaceutical Discovery, Pharmaceutical Drug Discovery, Pharmaceutical Industry Competitive Intelligence, Pharmaceutical R&D Investment, Pharmacogenomics, Precision Cancer Medicine, Rapid automation of plasma protein pools on June 15, 2026|

AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class II: 48 e-Books: English Edition & Spanish Edition. 152,000 pages downloaded under pay-per-view

Posted in AI Models in Healthcare, Artificial Intelligence - Breakthroughs in Theories and Technologies, Artificial Intelligence Applications in Health Care, Artificial Intelligence in Health Care - Tools & Innovations, Artificial Intelligence in Medicine - Applications in Therapeutics, Deep Learning, HealthCare IT, Intellectual Property, Innovations, Commercialization, Investment in technological breakthrough, IP Development by LPBI Group Team, LPBI Group, e-Scientific Media, DFP, R&D-M3DP, R&D-Drug Discovery, US Patents: SOPs and Team Management, Machine Learning, Natural Language Processing (NLP) on November 22, 2025| Leave a Comment »

AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class II: 48 e-Books: English Edition & Spanish Edition. 152,000 pages downloaded under pay-per-view

Curator: Aviva Lev-Ari, PhD, RN

We had researched the topic of AI Initiatives in Big Pharma in the following article:

- Authentic Relevance of LPBI Group’s Portfolio of IP as Proprietary Training Data Corpus for AI Initiatives at Big Pharma

We are publishing a Series of Five articles that demonstrate the Authentic Relevance of Five of the Ten Digital IP Asset Classes in LPBI Group’s Portfolio of IP for AI Initiatives at Big Pharma.

-

For the Ten IP Asset Classes in LPBI Group’s Portfolio, See

https://pharmaceuticalintelligence.com/portfolio-of-ip-assets/

The following Five Digital IP Asset classes are positioned as Proprietary Training Data and Inference for Foundation Models in Health care.

This Corpus comprises of Live Repository of Domain Knowledge Expert-Written Clinical Interpretations of Scientific Findings codified in the following five Digital IP ASSETS CLASSES:

• IP Asset Class I: Journal: PharmaceuticalIntelligence.com

6,250 scientific articles (70% curations, creative expert opinions. 30% scientific reports).

2.4MM Views, equivalent of $50MM if downloading an article is paid market rate of $30.

- PharmaceuticalIntelligence.com Journal – Projecting the Annual Rate of Article Views

• IP Asset Class II: 48 e-Books: English Edition & Spanish Edition.

152,000 pages downloaded under pay-per-view. The largest number of downloads for one e-Publisher (LPBI)

• IP Asset Class III: 100 e-Proceedings and 50 Tweet Collections of Top Biotech and Medical Global Conferences, 2013-2025

• IP Asset Class V: 7,500 Biological Images in our Digital Art Media Gallery, as prior art. The Media Gallery resides in WordPress.com Cloud of LPBI Group’s Web site

• IP Asset Class X: +300 Audio Podcasts: Interviews with Scientific Leaders

BECAUSE THE ABOVE ASSETS ARE DIGITAL ASSETS they are ready for use as Proprietary TRAINING DATA and INFERENCE for AI Foundation Models in HealthCare.

Expert‑curated healthcare corpus mapped to a living ontology, already packaged for immediate model ingestion and suitable for safe pre-training, evals, fine‑tuning and inference. If healthcare domain data is on your roadmap, this is a rare, defensible asset.

The article TITLE of each of the five Digital IP Asset Classes matched to AI Initiatives in Big Pharma, an article per IP Asset Class are:

- AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class I: PharmaceuticalIntelligence.com Journal, 2.5MM Views, 6,250 Scientific articles and Live Ontology

- AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class II: 48 e-Books: English Edition & Spanish Edition. 152,000 pages downloaded under pay-per-view

Article Conclusions by @grok:

Conclusions and ImplicationsLPBI’s e-books are “ready-to-ingest” for Big Pharma AI, enabling from efficiency gains to diagnostic breakthroughs. No prior comprehensive ML attempts highlight untapped value [by Big Pharma. However, we conducted in-house ML on two of the e-Books]; bilingual editions support global/equitable applications. Technical Implications: Powers multilingual small models for precision medicine. Business Implications: Fuels ROI on investments like Pfizer’s $500M push; licensing potential for partnerships. Unique Insight: In AI’s scale race, these assets provide a “rare moat” via curated human opus—unlike raw data, they embed clinical foresight for transformative inference. The article is promotional yet substantive, with dense Amazon links and calls to resources (e.g., BioMed e-Series page, IP portfolio). It builds on the prior Class I piece by shifting to long-form, creative text for deeper AI personalization.

- AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class III: 100 e-Proceedings and 50 Tweet Collections of Top Biotech and Medical Global Conferences, 2013-2025

- AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class V: 7,500 Biological Images in LPBI Group’s Digital Art Media Gallery, as prior art

- AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class X: +300 Audio Podcasts Library: Interviews with Scientific Leaders

In the series of five articles, as above, we are presenting the key AI Initiatives in Big Pharma as it was created by our prompt to @Grok on 11/18/2025:

- What are PFIZER’s AI INITIATIVES?

@Grok Response:

x.com/i/grok/share/0ol5VOJsEYs11baXq4xkzNb0h

| Generative AI tools that save scientists up to 16,000 hours annually in literature searches and data analysis. |

| Drug Discovery and Development Acceleration Pfizer uses AI, supercomputing, and ML to streamline R&D timelines |

| Clinical Trials and Regulatory Efficiency AI:

-Predictive Regulatory Tools -Decentralize Trials -inventory management |

| Disease Detection and Diagnostics:

– ATTR-CM Initiative – Rare diseases |

| Generative AI and Operational Tools:

– Charlie Platform – Scientific Data Cloud AWS powered ML on centralized data – Amazon’s SageMaker /Bedrock for Manufacturing efficiency – Global Health Grants: Pfizer Foundation’s AI Learning Lab for equitable access to care and tools for community care |

| Partnerships and Education

– Collaborations: IMI Big Picture for 3M – sample disease database – AI in Pharma AIPM Symposium: Drug discovery and Precision Medicine – Webinars of AI for biomedical data integration – Webinar on AI in Manufacturing |

| Strategic Focus:

– $500M R&D reinvestment by 2026 targets AI for Productivity – Part of $7.7B cost savings – Ethical AI, diverse DBs – Global biotech advances: China’s AI in CRISPR |

-

AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class II: 48 e-Books: English Edition & Spanish Edition. 152,000 pages downloaded under pay-per-view

The Left Column was written @Grok

The Right Column was written by Aviva Lev-Ari, PhD, RN

|

AI Initiative at Big Pharma i.e., Pfizer |

e-Books Domain-aware Editorials and Curations |

| Generative AI tools that save scientists up to 16,000 hours annually in literature searches and data analysis. | The electronic Table of Contents of every e-book is a CONCEPTUAL MASTER PIECE of one unique occurrence in Nature generated by the Editor, or the Editors that had

– Commissioned articles for the e-Book – Had selected articles from collections of Categories of Research created by domain knowledge experts – Had reviewed the TOTALITY of the Journal’s Ontology and found new concept to cover in the e-Book not originally planned – The vision of the Editor-in-Chief of the BioMed e-Series that reflects the BIG PICTURE of Patient care delivery. – UC, Berkeley PhD’83 – Knowledge student and Knowledge worker, 10/1970 to Present – Conceptual pioneer of 26 algorithms in Decision Science of Operations Management decision support tools – 2005 to Present in the Healthcare field. – 2005-2012: Clinical Nurse Manager in Post-acute SNF settings and Long-term Acute care Hospital Supervisor – had developed a unique view on Diagnosis, Therapeutics and Patient care delivery – The BioMed e-Series is the EPITOM of human CREATIVITY in Healthcare an OPUS MAGNUM created by collaboration of top Scientists, Physicians and MD/PhDs – The 48 e-Books Published by LPBI Group – represent the ONLY one Publisher on Amazon.com with +151,000 pages downloaded since the 1st e-book published and Pay-per-View was launched by Amazon.com in 2016. |

| Drug Discovery and Development Acceleration Pfizer uses AI, supercomputing, and ML to streamline R&D timelines | Two volumes on the BioMed e-Series were subjected to Medical Text Analysis with ML, Natural Language Processing (NLP).

– Cancer, Volume 1 (In English part of the Spanish Edition, Series C) – Genomics, Volume 2 (In English part of the Spanish Edition, Series B) – GPT capabilities are warranted to attempt to subject to ML every book of the MUTUALLY EXCLUSIVE 48 URLs provided by Amazon.com to LPBI Group, the Publisher. – 5 URLs for 5 Bundles in The English Edition: – Series A,B,C,D,E – English Edition – All books in each series – 5 Corpuses for domain-aware Small Language Model in English – All books in each series – 5 Corpuses for domain-aware Small Language Model in Spanish – 5 URLs for 5 Bundles in The Spanish Edition: – Series A,B,C,D,E –Spanish Edition

|

| Clinical Trials and Regulatory Efficiency AI:

-Predictive Regulatory Tools -Decentralize Trials -inventory management |

|

| Disease Detection and Diagnostics:

– ATTR-CM Initiative – Rare diseases |

– No one had attempted ML on every book, only two books were analyzed by ML.

– No one had attempted ML on all the Volumes in any of the 5 Series. – No one had attempted ML on all the 48 books – WHEN that will be done – a REVOLUTION on Disease Detection and Diagnostics will be seen for the first time

|

| Generative AI and Operational Tools:

– Charlie Platform – Scientific Data Cloud AWS powered ML on centralized data – Amazon’s SageMaker/Bedrock for Manufacturing efficiency – Global Health Grants: Pfizer Foundation’s AI Learning Lab for equitable access to care and tools for community care |

Add the content of all the Books to Charlie Platform |

| Partnerships and Education

Collaborations: IMI Big Picture for 3M – sample disease database

AI in Pharma AIPM Symposium: Drug discovery and Precision Medicine

Webinars of AI for biomedical data integration

Webinard on Ai in Manufacturing |

e-Books are the SOURCE for Education

– Offer the books as Partnership sustenance |

| Strategic Focus:

– $500M R&D reinvestment by 2026 targets AI for Productivity – Part of $7.7B cost savings – Ethical AI, diverse DBs – Global biotech advances: China’s AI in CRISPR |

URLs for the English-language Edition by e-Series:

Series A: Cardiovascular Diseases ($515) https://www.amazon.com/gp/product/B07P981RCS?ref_=dbs_p_mng_rwt_ser_shvlr&storeType=ebooks Series B: Frontiers in Genomics ($200) https://www.amazon.com/gp/product/B0BSDPG2RX?ref_=dbs_p_pwh_rwt_anx_b_lnk&storeType=ebooks Series C: Cancer & Oncology ($175) https://www.amazon.com/gp/product/B0BSDWVB3H?ref_=dbs_p_mng_rwt_ser_shvlr&storeType=ebooks Series D: Immunology ($325) https://www.amazon.com/gp/product/B08VVWTNR4?ref_=dbs_p_pwh_rwt_anx_b_lnk&storeType=ebooks Series E: Patient-Centered Medicine ($274) https://www.amazon.com/gp/product/B0BSDW2K6C?ref_=dbs_p_mng_rwt_ser_shvlr&storeType=ebooks

|

CONCLUSIONS: The Voice of Dr. Stephen J. Williams PhD

Article Summary of the ArticleTitle: by @grok

AI Initiatives in Big Pharma @Grok prompt & Proprietary Training Data and Inference by LPBI Group’s IP Asset Class II: 48 e-Books: English Edition & Spanish Edition. 152,000 pages downloaded under pay-per-view

Publication Date: November 22, 2025

Author/Curator: Aviva Lev-Ari, PhD, RN

(Posted by 2012pharmaceutical)

@Grok SOURCE:

Overview: This is the second installment in a five-article series on LPBI Group’s digital IP assets for AI in pharma. It focuses on IP Asset Class II—48 e-books (bilingual English/Spanish editions)—as a proprietary, expert-curated textual corpus for training and inference in healthcare AI models. Drawing from a November 18, 2025, Grok prompt on Pfizer’s AI efforts, the article maps e-book content to pharma applications, highlighting untapped ML/NLP potential for small language models. Unlike Class I (journal articles), this emphasizes long-form editorial creativity and bilingual scalability, positioning the assets as a “defensible moat” for Big Pharma’s AI acceleration.Main Thesis and Key Arguments

- Core Idea: LPBI’s e-books, with 152,000 pay-per-view downloads (largest for any single Amazon e-publisher since 2016), offer domain-specific, human-curated content (e.g., conceptual tables of contents as “masterpieces” reflecting patient care visions) that outperforms generic data in AI training. This enables precise inference for drug discovery, diagnostics, and efficiency, fostering human-AI synergy.

- Value Proposition: The BioMed e-Series (5 series: A-E, each bundled as a corpus) totals 48 volumes from collaborations with top scientists/MD/PhDs. Editor-in-Chief’s expertise (UC Berkeley PhD ’83, decision science algorithms, clinical nursing) infuses “big-picture” insights. Valued for multilingual models; only two volumes (Cancer Vol. 1, Genomics Vol. 2) have seen ML analysis—full application could “revolutionize” disease detection.

- Broader Context: Part of LPBI’s 10 IP classes; five (I, II, III, V, X) are AI-ready via living ontology. Contrasts with open-source data by emphasizing ethical, diverse, creative inputs for foundation models.

AI Initiatives in Big Pharma (Focus on Pfizer)Reuses the Grok prompt on Pfizer’s AI, with key highlights (verbatim from article’s table):

|

Initiative Category

|

Description

|

|---|---|

|

Generative AI Tools

|

Saves up to 16,000 hours annually in literature searches/data analysis.

|

|

Drug Discovery Acceleration

|

AI, supercomputing, ML to streamline R&D timelines.

|

|

Clinical Trials & Regulatory Efficiency

|

Predictive tools, decentralized trials, inventory management.

|

|

Disease Detection & Diagnostics

|

ATTR-CM Initiative, rare diseases focus.

|

|

Generative AI & Operational Tools

|

Charlie Platform; AWS-powered Scientific Data Cloud; SageMaker/Bedrock for manufacturing; Pfizer Foundation’s AI Learning Lab for equitable care.

|

|

Partnerships & Education

|

IMI Big Picture (3M sample disease database); AIPM Symposium (drug discovery/precision medicine); Webinars on AI for biomedical integration and manufacturing.

|

|

Strategic Focus

|

$500M R&D reinvestment by 2026 for AI productivity; part of $7.7B cost savings; ethical AI with diverse DBs; global advances (e.g., China’s CRISPR AI).

|

Mapping to LPBI’s Proprietary DataA core table aligns Pfizer initiatives with e-book alignments, showcasing ingestion for AI enhancement:

|

Pfizer AI Initiative

|

e-Books Alignment

|

|---|---|

|

Generative AI Tools (16,000 hours saved)

|

Electronic TOCs as conceptual masterpieces: Editor commissions/selections/ontology reviews reflect big-picture patient care (UC Berkeley PhD ’83, decision science pioneer, clinical experience); BioMed e-Series as opus magnum of human creativity; 48 e-books with 152,000+ downloads since 2016.

|

|

Drug Discovery Acceleration

|

ML/NLP applied to Cancer Vol. 1 (Series C) and Genomics Vol. 2 (Series B); Extend GPT to all 48 books via 5 English bundles (Series A-E) and 5 Spanish bundles as corpuses for domain-aware small language models.

|

|

Clinical Trials & Regulatory Efficiency

|

(No specific mapping provided.)

|

|

Disease Detection & Diagnostics (ATTR-CM, rare diseases)

|

Untapped: No prior ML on all books/volumes/series; Full analysis promises revolution in detection/diagnostics.

|

|

Generative AI & Operational Tools (Charlie, AWS, etc.)

|

Ingest all book content into Charlie Platform for centralized ML.

|

|

Partnerships & Education (IMI, AIPM, webinars)

|

e-Books as education source; Offer for partnership sustenance.

|

|

Strategic Focus ($500M reinvestment, ethics)

|

Bundles enable diverse, ethical DBs; URLs for English Series: A (Cardiovascular, $515): [link]; B (Genomics, $200): [link]; C (Cancer, $175): [link]; D (Immunology, $325): [link]; E (Patient-Centered, $274): [link]. Spanish equivalents implied.

|

Methodologies and Frameworks

- AI Training Pipeline: Package e-books (textual corpus) for pre-training (ontology-mapped ingestion), fine-tuning (e.g., ML on series bundles), and inference (e.g., diagnostics queries). Bilingual support for global models.

- ML/NLP Demo: Applied to two volumes; scale to 48 books via GPT for small language models (5 corpuses/language).

- Productivity Model: Amplifies Pfizer’s savings (16,000 hours, $7.7B total) by injecting expert creativity; ethical focus on diverse, compliant data for equity (e.g., AI Learning Lab).

- Insights: Quotes editor’s vision as “epitome of human creativity”; predicts full ML rollout as first-of-its-kind revolution, differing from Class I’s article-based ontology by focusing on editorial depth.

Conclusions and Implications

LPBI’s e-books are “ready-to-ingest” for Big Pharma AI, enabling from efficiency gains to diagnostic breakthroughs. No prior comprehensive ML attempts highlight untapped value [by Big Pharma. However, we conducted in-house ML on two of the e-Books]; bilingual editions support global/equitable applications. Technical Implications: Powers multilingual small models for precision medicine. Business Implications: Fuels ROI on investments like Pfizer’s $500M push; licensing potential for partnerships. Unique Insight: In AI’s scale race, these assets provide a “rare moat” via curated human opus—unlike raw data, they embed clinical foresight for transformative inference. The article is promotional yet substantive, with dense Amazon links and calls to resources (e.g., BioMed e-Series page, IP portfolio). It builds on the prior Class I piece by shifting to long-form, creative text for deeper AI personalization.

If you’d like comparisons across the series, deeper dives into specific e-books, or analysis of bilingual AI potential, just say the word!

1 web page

Bridging the Gender Gap in Healthcare: Unlocking Biopharma’s Potential in Women’s Health

Posted in AI Models in Healthcare, Artificial Intelligence Applications in Health Care, Artificial Intelligence in Health Care - Tools & Innovations, BioIT: BioInformatics, NGS, Clinical & Translational, Pharmaceutical R&D Informatics, Clinical Genomics, Cancer Informatics, Digital HealthCare – biotech & internet joint ventures, Electronic Health Record, Genetics & Pharmaceutical, Genomics Pharmacy, Glycobiology: Biopharmaceutical Production, Health Care System by Country, Health Economics and Outcomes Research, Health Law & Patient Safety, Health Law Policy, Healthcare costs and reimbursement, HealthCare IT, Healthcare Reform, Human Immune System in Health and in Disease, Mobile Healthcare, Personal Health Applications: Tech Innovations serves HealhCare, Pharmaceutical Analytics, Pharmaceutical Discovery, Pharmaceutical Drug Discovery, Pharmaceutical Industry Competitive Intelligence, Pharmaceutical R&D Informatics, Pharmaceutical R&D Investment, Pharmacogenomics, Population Health Management, Population Health Management, Genetics & Pharmaceutical, Population Health Management, Nutrition and Phytochemistry, Technology Transfer: Biotech and Pharmaceutical, Transformative Technologies in Healthcare, Voices of Patients and Healthcare Providers, Wearable Tech + Digital Health, Women Health, tagged advance therapy, Biopharmaceutical, gap, gender, Targeted therapy, translational therapy, womens' health on February 4, 2025| Leave a Comment »

Curator: Dr. Sudipta Saha, Ph.D.

Nearly half of the global population—and 80 percent of patients in therapeutic areas such as immunology—are women. Yet, treatments are frequently developed without tailored insights for female patients, often ignoring critical biological differences such as hormonal impacts, genetic factors, and cellular sex. Historically, women’s health has been narrowly defined through the lens of reproductive organs, while for non-reproductive conditions, women were treated as “small men.” This lack of focus on sex-specific biology has contributed to significant gaps in healthcare.

A recent analysis found that women spend 25 percent more of their lives in poor health compared with men due to the absence of sex-based treatments. Addressing this disparity could not only improve women’s quality of life but also unlock over $1 trillion in annual global GDP by 2040.

Four key factors contribute to the women’s health gap: limited understanding of sex-based biological differences, healthcare systems designed around male physiology, incomplete data that underestimates women’s disease burden, and chronic underfunding of female-focused research. For instance, despite women representing 78 percent of U.S. rheumatoid arthritis patients, only 7 percent of related NIH funding in 2019 targeted female-specific studies.

However, change is happening. Companies have demonstrated how targeted R&D can drive better outcomes for women. These therapies achieved expanded FDA approvals after clinical trials revealed their unique benefits for female patients. Similarly, addressing sex-based treatment gaps in asthma, atrial fibrillation, and tuberculosis could prevent millions of disability-adjusted life years.

By closing the women’s health gap, biopharma companies can drive innovation, improve therapeutic outcomes, and build high-growth markets while addressing long-standing inequities. This untapped opportunity holds the potential to transform global health outcomes for women and create a more equitable future.

References

Genomic data can predict miscarriage and IVF failure

Posted in Advanced Computing Platform, Artificial Intelligence - Breakthroughs in Theories and Technologies, Artificial Intelligence - General, Artificial Intelligence Applications in Health Care, Artificial Intelligence in Health Care - Tools & Innovations, Artificial Intelligence in Medicine - Application for Diagnosis, Artificial Intelligence in Medicine - Applications in Therapeutics, BioIT: BioInformatics, BioIT: BioInformatics, NGS, Clinical & Translational, Pharmaceutical R&D Informatics, Clinical Genomics, Cancer Informatics, Biological Engineering, Biological Networks, Biological Networks, Gene Regulation and Evolution, Biomarkers & Medical Diagnostics, Cell Level, Computational Biology/Systems and Bioinformatics, Computational Histopathology, Deep Learning in Pathology, Developmental biology, Diagnostics and Lab Tests, Digital HealthCare – biotech & internet joint ventures, Disease Biology, Genomic Testing: Methodology for Diagnosis, Genomics Pharmacy, HealthCare IT, Healthcare Reform, Machine Learning, MicroEngineering Cell-Tissue & Systems, Placenta, Preimplantation Genetic Diagnosis and Reproductive Genomics, Reproductive Andrology, Embryology, Genomic Endocrinology, Preimplantation Genetic Diagnosis and Reproductive Genomics, Reproductive Biology & Bio Instrumentation, therapeutics, Tissue Engineering, Translational Research, Women Health, tagged aneuploidy, Diagnosis, Genomic data, IVF, Miscarriage, treatment on June 15, 2022| Leave a Comment »

Reporter and Curator: Dr. Sudipta Saha, Ph.D.

Infertility is a major reproductive health issue that affects about 12% of women of reproductive age in the United States. Aneuploidy in eggs accounts for a significant proportion of early miscarriage and in vitro fertilization failure. Recent studies have shown that genetic variants in several genes affect chromosome segregation fidelity and predispose women to a higher incidence of egg aneuploidy. However, the exact genetic causes of aneuploid egg production remain unclear, making it difficult to diagnose infertility based on individual genetic variants in mother’s genome. Although, age is a predictive factor for aneuploidy, it is not a highly accurate gauge because aneuploidy rates within individuals of the same age can vary dramatically.

Researchers described a technique combining genomic sequencing with machine-learning methods to predict the possibility a woman will undergo a miscarriage because of egg aneuploidy—a term describing a human egg with an abnormal number of chromosomes. The scientists were able to examine genetic samples of patients using a technique called “whole exome sequencing,” which allowed researchers to home in on the protein coding sections of the vast human genome. Then they created software using machine learning, an aspect of artificial intelligence in which programs can learn and make predictions without following specific instructions. To do so, the researchers developed algorithms and statistical models that analyzed and drew inferences from patterns in the genetic data.

As a result, the scientists were able to create a specific risk score based on a woman’s genome. The scientists also identified three genes—MCM5, FGGY and DDX60L—that when mutated and are highly associated with a risk of producing eggs with aneuploidy. So, the report demonstrated that sequencing data can be mined to predict patients’ aneuploidy risk thus improving clinical diagnosis. The candidate genes and pathways that were identified in the present study are promising targets for future aneuploidy studies. Identifying genetic variations with more predictive power will serve women and their treating clinicians with better information.

References:

https://pubmed.ncbi.nlm.nih.gov/35347416/

https://pubmed.ncbi.nlm.nih.gov/31552087/

https://pubmed.ncbi.nlm.nih.gov/33193747/

Digital Therapeutics In Healthcare: The Market Perspectives

Posted in AI Models in Healthcare, Health Care System by Country, HealthCare IT, Prescription Drugs Costs, Technology Capital Expenses, United States on February 7, 2022| Leave a Comment »

Digital Therapeutics In Healthcare: The Market Perspectives

Reporter: Aviva Lev-Ari, PhD, RN

based on e-mail from

CB Insights <healthcare.insights@cbinsights.com> Thu, 20 Jan 2022 15:03:47 +0000

State Of Digital Health 2021 report

Breaking records and taking names

At the end of Q3’21, the digital health sector was on track to collect nearly $53B by the end of the year.

Fast-forward through Q4’21. Digital health startups surpassed that and pulled in a record-breaking $57.2B (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=3fa5150475&e=d62ca003c7) in funding in 2021, up 79% from 2020.

The US digital health market continued to dominate, reaching a record $37.9B (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=4e867a5607&e=d62ca003c7) in 2021.

In Q4’21 alone, the region collected $10.8B — more than Asia, the second-largest global market, recorded in all of 2021.

Within digital health, we saw 2 sectors take off in 2021:

Digital therapeutics (DTx) and

Mental health tech

Along with 127% funding growth compared to 2020, the DTx market (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=ca977c4de1&e=d62ca003c7) saw significant momentum, including increased business relationships (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=98081124d2&e=d62ca003c7) , expanding clinical evidence, and new regulatory approvals.

Want to go deeper into DTx?

Clients can download our DTx market map

Mental health tech also had a show-stopping year, with funding up 139% YoY (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=334bfe3143&e=d62ca003c7) to reach $5.5B.

But we are still in early innings. With 68% of 2021 deals being early-stage, there is room for growth in the mental health tech space.

Want to go deeper? Clients can download our mental health tech market map here (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=57dacdc7a2&e=d62ca003c7) .

Here are a few more notable trends covered in the report:

* What happened in healthcare IT (page 131 (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=e60dc58576&e=d62ca003c7) )? Will this continue in 2022?

* In Q4, US digital health funding (page 146 (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=97b46b9d4e&e=d62ca003c7) ) hit an all-time high, even though deals sank to a low for the year (it’s typical to see fewer deals in Q4 due to the holidays).

* While M&A exits (pages 65-66 (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=dd55fc09b0&e=d62ca003c7) ) soared in 2021 on the whole, they dipped meaningfully in Q4 (this has not been historically seasonal).

If you want to see how your favorite sector performed, check out the “Collection Spotlights” section, which begins on page 83 (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=360bcc7859&e=d62ca003c7) .

Preliminary survey results

Earlier this month we surveyed our audience for 2022 healthcare predictions. We plan to unveil the responses in the next newsletter.

Until then, I wanted to share the results of our bonus question, ”When will you wake up and not think about Covid?”

Nearly half (44%) of our audience picked “After 2023,” which is a big change from June 2021, when just 18% of you selected that option.

Stay healthy,

Marc Albanese (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=a6f2990166&e=d62ca003c7)

P.S. Thank you to Amanda (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=d4b485d71f&e=d62ca003c7) and Nicole (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=117de54447&e=d62ca003c7) for your help compiling the newsletter this week!

P.P.S. Are you looking for the best place to write data-driven healthcare research? We are hiring for a senior analyst on our healthcare team (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=4d78da1730&e=d62ca003c7) .

CB INSIGHTS HITS

Healthcare Research: Startups, Trends, Tech Solutions & More. (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=951a587727&e=d62ca003c7)

Here’s a sample of our digital health and healthcare research on the sector’s investment and funding trends, business models, tech solutions, and more. Read it here (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=82c24532c1&e=d62ca003c7) .

[Client Research] Tech Market Map Report —

Digital Therapeutics In Healthcare.

This report highlights 150 digital therapeutics companies that are addressing 15 distinct therapeutic areas, from smoking cessation to anxiety and depression. Read it here (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=ebb1bd80f3&e=d62ca003c7) .

[Client Research] Why Healthcare Providers Are Prioritizing Digital Patient Payments. (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=f5511b9a5b&e=d62ca003c7)

Digital patient payments have garnered high market momentum and widespread industry leader activity in the revenue cycle management space — making it an industry worth prioritizing. Read it here (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=7f5edfb70f&e=d62ca003c7) .

[Client Research] Tech Market Map Report — Clinical Trials In Healthcare. (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=983995d94d&e=d62ca003c7) This report looks at the clinical trials tech companies serving pharmaceutical companies and CROs. Read it here (https://cbinsights.us1.list-manage.com/track/click?u=0c60818e26ecdbe423a10ad2f&id=e0c17d0cec&e=d62ca003c7) .

SOURCE

based on e-mail from

CB Insights <healthcare.insights@cbinsights.com> Thu, 20 Jan 2022 15:03:47 +0000

IBM has reached an agreement to sell its Watson Health data and analytics business to the private-equity firm Francisco Partners

Posted in AI Models in Healthcare, Artificial Intelligence - General, Artificial Intelligence Applications in Health Care, HealthCare IT, United States on January 26, 2022| Leave a Comment »

IBM has reached an agreement to sell its Watson Health data and analytics business to the private-equity firm Francisco Partners

Reporter: Aviva Lev-Ari, PhD, RN

UPDATED on 2/5/2022

UPDATED on 1/31/2022

AI Hot in Healthcare Despite IBM’s Watson Health Pullout

28/01/2022

- Big pharma companies are snapping up collaborations with firms using AI to speed up drug discovery, with one of the latest being Sanofi’s pact with Exscientia.

- Tech giants are placing big bets on digital health analysis firms, such as Oracle’s €25.42B ($28.3B) takeover of Cerner in the US.

- There’s also a steady flow of financing going to startups taking new directions with AI and bioinformatics, with the latest example being a €20M Series A round by SeqOne Genomics in France.

“IBM Watson uses a philosophy that is diametrically opposed to SeqOne’s,” said Jean-Marc Holder, CSO of SeqOne. “[IBM Watson seems] to rely on analysis of large amounts of relatively unstructured data and bet on the volume of data delivering the right result. By opposition, SeqOne strongly believes that data must be curated and structured in order to deliver good results in genomics.”

UPDATED on 1/31/2022

Key M&A in Health IT include:

Last month,

- IBM arch-rival Oracle announced a $28 billion takeover of electronic health record company Cerner, while 2021 also saw

- Microsoft’s $19.7 billion play for AI specialist Nuance and a

- $17 billion takeover of Athenahealth by investment groups Bain Capital and Hellman & Friedman.

IBM sells off large parts of Watson Health business

January 24, 2022

Francisco Partners is picking up a range of databases and analytics tools – including

- Health Insights,

- MarketScan,

- Clinical Development,

- Social Programme Management,

- Micromedex and

- other imaging and radiology tools, for an undisclosed sum estimated to be in the region of $1 billion.

IBM said the sell-off is tagged as “a clear next step” as it focuses on its platform-based hybrid cloud and artificial intelligence strategy, but it’s no secret that Watson Health has failed to live up to its early promise.

The sale also marks a retreat from healthcare for the tech giant, which is remarkable given that it once said it viewed health as second only to financial services market as a market opportunity.

IBM said it “remains committed to Watson, our broader AI business, and to the clients and partners we support in healthcare IT.”

The company reportedly invested billions of dollars in Watson, but according to a Wall Street Journal report last year, the health business – which provided cloud-based access to the supercomputer and a range of analytics services – has struggled to build market share and reach profitability.

An investigation by Stat meanwhile suggested that Watson Health’s early push into cancer for example was affected by a premature launch, interoperability challenges and over-reliance on human input to generate results.

For its part, IBM has said that the Watson for Oncology product has been improving year-on-year as the AI crunches more and more data.

That is backed up by a meta analysis of its performance published last year in Nature found that the treatment recommendations delivered by the tool were largely in line with human doctors for several cancer types.

However, the study also found that there was less consistency in more advanced cancers, and the authors noted the system “still needs further improvement.”

Watson Health offers a range of other services of course, including

- tools for genomic analysis and

- running clinical trials that have found favour with a number of pharma companies.

- Francisco said in a statement that it offers “a market leading team [that] provides its customers with mission critical products and outstanding service.”

The deal is expected to close in the second quarter, with the current management of Watson Health retaining “similar roles” in the new standalone company, according to the investment company.

IBM’s step back from health comes as tech rivals are still piling into the sector.

SOURCE

https://pharmaphorum.com/news/ibm-sells-off-large-parts-of-watson-health-business/

@pharma_BI is asking: What will be the future of WATSON Health?

@AVIVA1950 says on 1/26/2022:

Aviva believes plausible scenarios will be that Francisco Partners will:

A. Invest in Watson Health – Like New Mountains Capital (NMC) did with Cytel

B. Acquire several other complementary businesses – Like New Mountains Capital (NMC) did with Cytel

C. Hold and grow – Like New Mountains Capital (NMC) is doing with Cytel since 2018.

D. Sell it in 7 years to @Illumina or @Nvidia or Google’s Parent @AlphaBet

1/21/2022

IBM said Friday it will sell the core data assets of its Watson Health division to a San Francisco-based private equity firm, marking the staggering collapse of its ambitious artificial intelligence effort that failed to live up to its promises to transform everything from drug discovery to cancer care.

https://www.statnews.com/2022/01/21/ibm-watson-health-sale-equity/

IBM has reached an agreement to sell its Watson Health data and analytics business to the private-equity firm Francisco Partners. … He said the deal will give Francisco Partners data and analytics assets that will benefit from “the enhanced investment and expertise of a healthcare industry focused portfolio.”5 days ago

IBM Is Selling Watson Health Unit to Private-Equity Firmhttps://www.barrons.com › articles › ibm-selling-watson-h…About featured snippets•Feedback

IBM is selling off Watson Health to a private equity firm.https://www.nytimes.com › 2022/01/21 › business › ibm-…

5 days ago — IBM has been trying to find buyers for the Watson Health business for more than a year. And it was seeking a sale price of about $1 billion, The …Missing: Statement | Must include: Statement

5 days ago — International Business Machines Corp. agreed to sell part of its IBM Watson Health business to private equity firm Francisco Partners, …

IBM has sold Watson Health. It was a long time coming.https://www.protocol.com › bulletins › ibm-watson-heal…

5 days ago — IBM announced today that it has sold its Watson Health data and analytics assets to private equity firm Francisco Partners.

IBM to sell Watson Health assets to Francisco Partnershttps://www.healthcareitnews.com › news › ibm-sell-wa…

5 days ago — IBM on Friday announced a deal with Bay Area-based Francisco Partners to sell off healthcare data and analytics assets from its Watson …

IBM is selling off its Watson Health assets – CNNhttps://www.cnn.com › 2022/01/21 › tech › ibm-selling-w…

5 days ago — IBM said Friday that it will sell off the healthcare data and analytics assets housed under its Watson Health unit to private equity firm …

IBM to sell Watson Health division to private equity firmhttps://www.healthcaredive.com › news › ibm-sell-wats…

5 days ago — Tom Rosamilia, senior vice president of IBM Software, said in a statement the deal is a next step allowing IBM to focus more intensely on its …

IBM sells Watson Health assets to investment firm Francisco …https://www.fiercehealthcare.com › tech › ibm-sells-wat…

5 days ago — IBM has reached a deal to sell the healthcare data and analytics assets from its Watson Health business to investment firm Francisco …

Francisco Partners to Acquire IBM’s Healthcare Data and …https://newsroom.ibm.com › 2022-01-21-Francisco-Par…

5 days ago — “IBM remains committed to Watson, our broader AI business, and to the clients and partners we support in healthcare IT.Missing: Statement | Must include: Statement

IBM Sells Portion of Watson Health Business to Francisco …https://www.channele2e.com › ChannelE2E Blog

5 days ago — IBM Watson Health – Certain Assets Sold: Executive Perspectives. In a prepared statement about the deal, Tom Rosamilia, senior VP, IBM Software, …

5 days ago — Another IBM executive, Tom Rosamilia, a senior vice president with IBM Software, said in a statement that the sale of the Watson Health assets …

Francisco Partners scoops up bulk of IBM’s Watson Health unithttps://techcrunch.com › 2022/01/21 › francisco-partne…

5 days ago — In what has to be considered an anticlimactic ending, IBM sold off the data assets of its Watson Health unit to private equity firm …

IBM Sells Some Watson Health Assets for More Than $1 Billionhttps://www.bloombergquint.com › Business

IBM confirmed an earlier Bloomberg report on the sale in a statement on Friday, … “IBM remains committed to Watson, our broader AI business, and to the …

IBM offloads Watson Health business data, analyticshttps://searchbusinessanalytics.techtarget.com › news › IB…

5 days ago — IBM has sold the bulk of its Watson Health data and analytics business to a … In a press statement, IBM said offloading its Watson Health …

IBM selling Watson Health data and analytics business to …https://digitalhealth.modernhealthcare.com › Finance

5 days ago — IBM announced Friday that Francisco Partners will acquire its … The news comes after IBM sold three components of its Watson Health …

IBM to sell Watson Health assets to private equity firmhttps://www.auntminnie.com › …

5 days ago — IBM has agreed to sell healthcare data analytics assets from its current Watson Health business to private equity firm Francisco Partners.

IBM sells off large parts of Watson Health business -https://pharmaphorum.com › news › ibm-sells-off-large…

2 days ago — Tech giant IBM draws back from its digital health aspirations, agreeing a deal to sell a large chunk of IBM Watson Health to private equity …

IBM sells off Watson AI healthcare unit – Verdicthttps://www.verdict.co.uk › ibm-sells-off-watson-ai-hea…

2 days ago — IBM is to sell off its Watson Health data assets, bringing all but the final blow to … Senior Vice President, IBM Software in a statement.

IBM Sells Portions Of Watson Health Unit To Investment Firmhttps://www.investors.com › news › technology › ibm-s…

5 days ago — The sale to Francisco Partners is the latest step by IBM to refocus its … said IBM senior vice president Tom Rosamilia in a statement.

5 days ago — 5, IBM (NYSE: IBM) initially explored putting IBM Watson Health up for sale in … senior vice president of IBM Software, in a statement.

IBM is selling off its Watson Health assets – KESQhttps://kesq.com › money › 2022/01/21 › ibm-is-selling…

5 days ago — “The Watson Health sale has been anticipated for quite some time,” Paddy … senior vice president of IBM Software, said in a statement.

Report: IBM seeking to sell Watson Health unit for $1B+https://siliconangle.com › 2022/01/06 › report-ibm-see…

Jan 6, 2022 — IBM Corp. has launched a new effort to sell its Watson Health division, Axios reported on Wednesday, and the company is said to be hoping …

History of IBM – Wikipediahttps://en.wikipedia.org › wiki › History_of_IBM As the sales force grew into a highly professional and knowledgeable arm of the company, Watson focused their attention on providing large-scale tabulating …

Remember IBM’s Amazing Watson AI? Now it’s desperately …https://almooon.com › remember-ibms-amazing-watson…

Jan 7, 2022 — IBM’s infamous Watson artificial intelligence once defeated two $1 … offering the health portion of its much-hyped algorithm for sale.

IBM shifts focus with sale of Watson marketing, commerce …https://www.marketingdive.com › news › ibm-shifts-foc…

Apr 9, 2019 — IBM plans to sell its Watson marketing and commerce solutions to the private equity firm Centerbridge Partners, the company announced in a …

IBM and Salesforce Join Forces to Bring Watson and Einstein …http://www.smartcustomerservice.com › News-Features

Jan 26, 2018 — IBM has, meanwhile, named Salesforce its preferred customer engagement platform for sales and service. “The combination of IBM Cloud and …

IBM Sells Watson Health Assets to Investment Firm – WSJhttps://www.wsj.com › articles › ibm-sells-watson-health-a…

5 days ago — International Business Machines Corp. IBM 5.65% agreed to sell the data and analytics assets from its Watson Health business to investment …Missing: Statement | Must include: Statement

Latest News & Videos, Photos about ibm watson health – The …https://economictimes.indiatimes.com › topic › ibm-wat… IBM is said to consider sale of Watson Health amid cloud focus … Research India and CTO IBM India /South Asia, was quoted as saying in an IBM statement.

IBM explores sale of Watson Health | Fox Businesshttps://www.foxbusiness.com › healthcare › ibm-explores-…

Feb 18, 2021 — International Business Machines Corp. is exploring a potential sale of its IBM Watson Health business, according to people familiar with the …

IBM Explores Sale of IBM Watson Health – Slashdothttps://slashdot.org › story › ibm-explores-sale-of-ibm-…

Feb 19, 2021 — IBM is exploring a potential sale of its IBM Watson Health business, WSJ is reporting, citing people familiar with the matter, …

Watson Applications Software Sales Specialist | IBM Careershttps://krb-sjobs.brassring.com › HomeWithPreLoad

Job Details: Do you have experience helping clients implement innovative enterprise technology solutions that help them sol.

Georgia Watson – Sales Enablement Festivalhttps://festival2021.salesenablementcollective.com › ge…

Working for IBM as a Sales Enablement and Skills Transformation lead, Georgia was recently recognized as an Innovator of the Year in the International Business …

IBM’s Watson Health is sold off in parts | Hacker Newshttps://news.ycombinator.com › item

3 days ago — Please don’t make such definite statements. You even say it in your own comment … People outside tech were buzzing about IBM and Watson.

Data Before Technology: IBM Watson’s Vision – Forresterhttps://www.forrester.com › Featured Blogs

Nov 2, 2014 — I sat down with Steve Cowley, General Manager for IBM Watson, on Tuesday at … Steve surprised me with this statement, “[With] traditional …

How IBM Watson Overpromised and Underdelivered on AI …https://spectrum.ieee.org › how-ibm-watson-overpromised…After its triumph on Jeopardy!, IBM’s AI seemed poised to revolutionize medicine. Doctors are still waiting.

You’re probably using IBM’s Watson computer and don’t know ithttps://www.vox.com › ibm-ginni-rometty-watson

Jun 1, 2016 — But please don’t call it “artificial intelligence,” IBM’s CEO says. … sales figures aren’t yet disclosed in its financial statements.

IBM is selling off its Watson Health assets – KYMAhttps://kyma.com › news › 2022/01/21 › ibm-is-selling-…

5 days ago — “The Watson Health sale has been anticipated for quite some time,” Paddy … senior vice president of IBM Software, said in a statement.

IBM, investment firm reach deal for Watson Health assetshttps://www.mmm-online.com › home › channel › brea…

5 days ago — IBM will sell the healthcare data and analytics assets of its Watson Health business to investment firm Francisco Partners as part of a deal …

IBM has sold off Watson at a steep discount, and is exiting the …https://www.reddit.com › Futurology › comments › ib…

3 days ago — Nuance played a part in building watson in supplying the speech recognition component of Watson. Through the years, Nuance has done some serious …

2021 Gartner BI Magic Quadrant – Download the Full ReportAd·https://www.qlik.com/compare/watsonQlik® Is Named a Leader in the 2021 Gartner Magic Quadrant for Analytics and BI Platforms. Looking for a Trusted Data Analytics Platform? Discover the Difference with…BI & Data Trends for 2022 · Gartner Magic Quadrant · BI & Analytics Survey 22

Can the Public Benefit Company Structure Save US Healthcare?

Posted in Accountable Care Organizations, Affordable Care Act, and Bioethics, Centers for Medicare & Medicaid Services, Federal Budget Appropriations, Health Care System by Country, Health Economics and Outcomes Research, Health Law & Patient Safety, Health Law Policy, Healthcare costs and reimbursement, HealthCare IT, Healthcare Reform, Hospital reputation, Law and Medicine Conflicts, Leadership, Power, Social Interlocking Connections, Patient Experience, Patient Outlook, Population Health Management, Population Health Management, Genetics & Pharmaceutical, Support Staff, U.S. Employment-to-Population Ratio, United States, Value-based Drug Pricing, tagged aca, Affordable Healthcare Act, health economics, healthcare, healthcare cost, healthinequity, Medicaid, medical costs, medicare costs, Patient care, public benefit company, rural healthcare on August 20, 2021| Leave a Comment »

Can the Public Benefit Company Structure Save US Healthcare?

Curator: Stephen J. Williams, Ph.D.

UPDATED 11/05/2023

Public Benefit Corporation structure in healthcare has actually been around since the 1970s in New Yourk State, when New York City’s new Health and Hospitals Corporation took over the city Department of Hospitals and today runs 11 hospitals and four long-term care facitlites in the city. The following link to an article describes however the problems occuring with Nassau and Westchester hosptial systems, which were converted to New York PBC status in the 1990s. As the article states the financial problems in 2004 which these hospitals encountered

do not stem from their unusual status as public benefit corporations, and might have been even worse off had they not converted

The New York Times article of 2004 “At 2 Hospitals, Fiscal Troubles in the Glare of Public View” highlight in fact the growing problem that all hospitals are encountering, especially on the fiscal side. But it does highlight how to better structure these entities and why full commitment to the PBC structure is necessary.

In 2003 New York State had a record closure of hospitals, and in 2004 Nassau and WestChester were having such fiscal problems it threatened the bond status of those counties. Despite the regular problems hospitals had, critics had said there were two major contributing factors to their woes

- the two agencies had not completed their transition from government operations to fully competitve hospitals

- as a PBC they bear a costly mission of serving the uninsured

As a PBC the structure allows one to shed cumbersome government rules, giving them the flexibility to conduct business like other hospitals.

In addition they are no longer dependent, in fact now forced, to forgo dependence on public funding and look for independent means of investment. With their semi-independence from government the agencies also are more insulted from political pressure.

However this seemed to be the problem. These agencies were still to dependent on their local government and there was still local political influence on their boards.

UPDATED 3/15/2023

According to Centers for Medicare and Medicare Services (CMS.gov) healthcare spending per capita has reached 17.7 percent of GDP with, according to CMS data:

From 1960 through 2013, health spending rose from $147 per person to $9,255 per person, an average annual increase of 8.1 percent.

the National Health Expenditure Accounts (NHEA) are the official estimates of total health care spending in the United States. Dating back to 1960, the NHEA measures annual U.S. expenditures for health care goods and services, public health activities, government administration, the net cost of health insurance, and investment related to health care. The data are presented by type of service, sources of funding, and type of sponsor.

U.S. health care spending grew 4.6 percent in 2019, reaching $3.8 trillion or $11,582 per person. As a share of the nation’s Gross Domestic Product, health spending accounted for 17.7 percent.

And as this spending grew (demand for health care services) associated costs also rose but as the statistical analyses shows there was little improvement in many health outcome metrics during the same time.

It appears that US healthcare may be on the precipice of a transformational shift, but what will this shift look like? The following post examines if the corporate structure of US healthcare needs to be changed and what role does a Public Benefit Company have in this much needed transformation.

Hippocratic Oath

I swear by Apollo the physician, and Asclepius, and Hygieia and Panacea and all the gods and goddesses as my witnesses, that, according to my ability and judgement, I will keep this Oath and this contract:

To hold him who taught me this art equally dear to me as my parents, to be a partner in life with him, and to fulfill his needs when required; to look upon his offspring as equals to my own siblings, and to teach them this art, if they shall wish to learn it, without fee or contract; and that by the set rules, lectures, and every other mode of instruction, I will impart a knowledge of the art to my own sons, and those of my teachers, and to students bound by this contract and having sworn this Oath to the law of medicine, but to no others.

I will use those dietary regimens which will benefit my patients according to my greatest ability and judgement, and I will do no harm or injustice to them.

I will not give a lethal drug to anyone if I am asked, nor will I advise such a plan; and similarly I will not give a woman a pessary to cause an abortion.

In purity and according to divine law will I carry out my life and my art.

I will not use the knife, even upon those suffering from stones, but I will leave this to those who are trained in this craft.

Into whatever homes I go, I will enter them for the benefit of the sick, avoiding any voluntary act of impropriety or corruption, including the seduction of women or men, whether they are free men or slaves.

Whatever I see or hear in the lives of my patients, whether in connection with my professional practice or not, which ought not to be spoken of outside, I will keep secret, as considering all such things to be private.

So long as I maintain this Oath faithfully and without corruption, may it be granted to me to partake of life fully and the practice of my art, gaining the respect of all men for all time. However, should I transgress this Oath and violate it, may the opposite be my fate.

Translated by Michael North, National Library of Medicine, 2002.

Much of the following information can be found on the Health Affairs Blog in a post entitled

Public Benefit Corporations: A Third Option For Health Care Delivery?

By Soleil Shah, Jimmy J. Qian, Amol S. Navathe, Nirav R. Shah

Limitations of For Profit and Non-Profit Hospitals

For profit represent ~ 25% of US hospitals and are owned and governed by shareholders, and can raise equity through stock and bond markets.

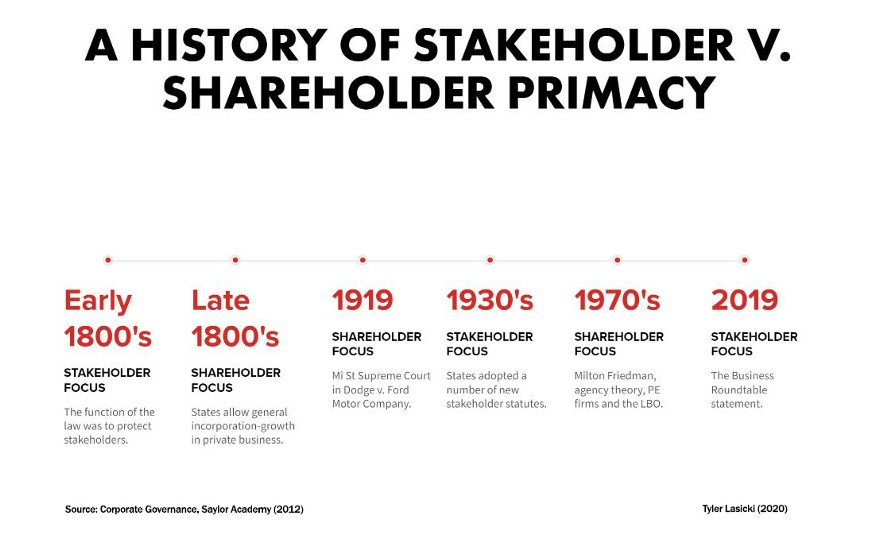

According to most annual reports, the CEOs incorrectly assume they are legally bound as fiduciaries to maximize shareholder value. This was a paradigm shift in priorities of companies which started around the mid 1980s, a phenomenon discussed below.

A by-product of this business goal, to maximize shareholder value, is that CEO pay and compensation is naturally tied to equity markets. A means for this is promoting cost efficiencies, even in the midst of financial hardships.

A clear example of the failure of this system can be seen during the 2020- current COVID19 pandemic in the US. According to the Medicare Payment Advisory Commission, four large US hospitals were able to decrease their operating expenses by $2.3 billion just in Q2 2020. This amounted to 65% of their revenue; in comparison three large NONPROFIT hospitals reduced their operating expense by an aggregate $13 million (only 1% of their revenue), evident that in lean times for-profit will resort to drastic cost cutting at expense of service, even in times of critical demands for healthcare.

Because of their tax structure and perceived fiduciary responsibilities, for-profit organizations (unlike non-profit and public benefit corporations) are not legally required to conduct community health need assessments, establish financial assistance policies, nor limit hospital charges for those eligible for financial assistance. In addition to the difference in tax liability, for-profit, unlike their non-profit counterparts, at least with hospitals, are not funded in part by state or local government. As we will see, a large part of operating revenue for non-profit university based hospitals is state and city funding.

Therefore risk for financial responsibility is usually assumed by the patient, and in worst case, by the marginalized patient populations on to the public sector.

Tax Structure Considerations of for-profit healthcare

Financials of major for-profit healthcare entities (2020 annual)

Non-profit Healthcare systems

Nonprofits represent about half of all hospitals in the US. Most of these exist as a university structure, so retain the benefits of being private health systems and retaining the funding and tax benefits attributed to most systems of higher education. And these nonprofits can be very profitable. After taking in consideration the state, local, and federal tax exemptions these nonprofits enjoy, as well as tax-free donations from contributors (including large personal trust funds), a nonprofit can accumulate a large amount of revenue after expenses. In fact 82 nonprofit hospitals had $33 billion of net asset increase year-over-year (20% increase) from 2016 to 2017. The caveat is that this revenue over expenses is usually spent on research or increased patient services (this may mean expanding the physical infrastructure of the hospital or disseminating internal grant money to clinical investigators, expanding the hospital/university research assets which could result in securing even larger amount of external funding from government sources.

And although this model may work well for intercity university/healthcare systems, it is usually a struggle for the rural nonprofit hospitals. In 2020, ten out of 17 rural hospitals that went under were nonprofits. And this is not just true in the tough pandemic year. Over the past two decades multitude of nonprofit rural hospitals had to sell and be taken over by larger for-profit entities.

Hospital consolidation has led to a worse patient experience and no real significant changes in readmission or mortality data. (The article below is how over 130 rural hospitals have closed since 2010, creating a medical emergency in rural US healthcare)

https://www.nationalgeographic.com/history/article/appalachian-hospitals-are-disappearing

And according to the article below it is only to get worse

The authors of the Health Affairs blog feel a major disadvantage of both the for-profit and non-profit healthcare systems is “that both face limited accountability with respect to anticompettive mergers and acquisitions.”

More hospital consolidation is expected post-pandemic

Aug 10, 2020

By Rich Daly, HFMA Senior Writer and Editor

News | Coronavirus

More hospital consolidation is expected post-pandemic

- Hospital deal volume is likely to accelerate due to the financial damage inflicted by the coronavirus pandemic.

- The anticipated increase in volume did not show up in the latest quarter, when deals were sharply down.

- The pandemic may have given hospitals leverage in coming policy fights over billing and the creation of “public option” health plans.

Hospital consolidation is likely to increase after the COVID-19 pandemic, say both critics and supporters of the merger-and-acquisition (M&A) trend.

The financial effects of the coronavirus pandemic are expected to drive more consolidation between and among hospitals and physician practices, a group of policy professionals told a recent Washington, D.C.-based web briefing sponsored by the Alliance for Health Policy.

“There is a real danger that this could lead to more consolidation, which if we’re not careful could lead to higher prices,” said Karyn Schwartz, a senior fellow at the Kaiser Family Foundation (KFF).

Schwartz cited a recent KFF analysis of available research that concluded “provider consolidation leads to higher health care prices for private insurance; this is true for both horizontal and vertical consolidation.”

Kenneth Kaufman, managing director and chair of Kaufman Hall, noted that crises tend to push financially struggling organizations “further behind.”

“I wouldn’t be surprised at all if that happens,” Kaufman said. “That will lead to further consolidation in the provider market.”

The initial rounds of federal assistance from the CARES Act, which were based first on Medicare revenue and then on net patient revenue, may fuel consolidation, said Mark Miller, PhD, executive vice president of healthcare for Arnold Ventures. That’s because the funding formulas favored organizations that already had higher revenues, he said, and provided less assistance to low-revenue organizations.

HHS has distributed $116.2 billion from the $175 billion in provider funding available through the CARES Act and the Paycheck Protection Program and Health Care Enhancement Act. The largest distributions used the two revenue formulas cited by Miller.

No surge in M&A yet

The expected burst in hospital M&A activity has yet to occur. Kaufman Hall identified 14 transactions in the second quarter of 2020, far fewer than in the same quarter in any of the four preceding years, when second-quarter transactions totaled between 19 and 31. The latest deals were not focused on small hospitals, with average seller revenue of more than $800 million — far larger than the previous second-quarter high of $409 million in 2018.

Six of the 14 announced transactions were divestitures by major for-profit health systems, including Community Health Systems, Quorum and HCA.

Kaufman Hall’s analysis of the recent deals identified another pandemic-related factor that may fuel hospital M&A: closer ties between hospitals. The analysis cited the example of Lifespan and Care New England, which had suspended merger talks in 2019. More recently, in a joint announcement, the CEOs of the two systems noted that because of the COVID-19 crisis, the two systems “have been working together in unprecedented ways” and “have agreed to enter into an exploration process to understand the pros and cons of what a formal continuation of this collaboration could look like in the future.”

The M&A outlook for rural hospitals

The pandemic has had less of a negative effect on the finances of rural hospitals that previously joined larger health systems, said Suzie Desai, senior director of not-for-profit healthcare for S&P Global.

A CEO of a health system with a large rural network told Kaufman the federal grants that the system received for its rural hospitals were much larger than the grants paid through the general provider fund.

“If that was true across the board, then the federal government recognized that many rural hospitals could be at risk of not being able to make payroll; actually running out of money,” Kaufman said. “And they seem to have bent over backwards to make sure that didn’t happen.”

Other CARES Act funding distributed to providers included:

- $12.8 billion for 959 safety net hospitals

- $11 billion to almost 4,000 rural healthcare providers and hospitals in urban areas that have certain special rural designations in Medicare

Telehealth has helped rural hospitals but has not been sufficient to address the financial losses inflicted by the pandemic, Desai said.

Other coming trends include a sharper cost focus

Desai expects an increasing focus “over the next couple years” on hospital costs because of the rising share of revenue received from Medicare and Medicaid. She expects increased efforts to use technology and data to lower costs.

Billy Wynne, JD, chairman of Wynne Health Group, expects telehealth restrictions to remain relaxed after the pandemic.

Also, the perceptions of the public and politicians about the financial health of hospitals are likely to give those organizations leverage in coming policy fights over changes such as banning surprise billing and creating so-called public-option health plans, Wynne said. As an example, he cited the Colorado legislature’s suspension of the launch of a public option “in part because of sensitivities around hospital finances in the COVID pandemic.”

“Once the dust settles, it’ll be interesting to see if their leverage has increased or decreased due to what we’ve been through,” Wynne said.

About the Author

Rich Daly, HFMA Senior Writer and Editor,

is based in the Washington, D.C., office. Follow Rich on Twitter: @rdalyhealthcare

Source: https://www.hfma.org/topics/news/2020/08/more-hospital-consolidation-is-expected-post-pandemic.html

From Harvard Medical School

Hospital Mergers and Quality of Care

A new study looks at the quality of care at hospitals acquired in a recent wave of consolidations

By JAKE MILLER January 16, 2020 Research

Image: NirutiStock / iStock / Getty Images Plus

The quality of care at hospitals acquired during a recent wave of consolidations has gotten worse or stayed the same, according to a study led by Harvard Medical School scientists published Jan. 2 in NEJM.

The findings deal a blow to the often-cited arguments that hospital consolidation would improve care. A flurry of earlier studies showed that mergers increase prices. Now after analyzing patient outcomes after hundreds of hospital mergers, the new research also dashes the hopes that this more expensive care might be of higher quality.

Get more HMS news here

“Our findings call into question claims that hospital mergers are good for patients—and beg the question of what we are getting from higher hospital prices,” said study senior author J. Michael McWilliams, the Warren Alpert Foundation Professor of Health Care Policy in the Blavatnik Institute at HMS and an HMS professor of medicine and a practicing general internist at Brigham and Women’s Hospital.

McWilliams noted that rising hospital prices have been one of the leading drivers of unsustainable growth in U.S. health spending.

To examine the impact of hospital mergers on quality of care, researchers from HMS and Harvard Business School examined patient outcomes from nearly 250 hospital mergers that took place between 2009 and 2013. Using data collected by the Centers for Medicare and Medicaid Services, they analyzed variables such as 30-day readmission and mortality rates among patients discharged from a hospital, as well as clinical measures such as timely antibiotic treatment of patients with bacterial pneumonia. The researchers also factored in patient experiences, such as whether those who received care at a given hospital would recommend it to others. For their analysis, the team compared trends in these indicators between 246 hospitals acquired in merger transactions and unaffected hospitals.

The verdict? Consolidation did not improve hospital performance, and patient-experience scores deteriorated somewhat after the mergers.

The study was not designed to examine the reasons behind the worsening in patient experience. Weakening of competition due to hospital mergers could have contributed, the researchers said, but deeper exploration suggested other potential mechanisms. Notably, the analysis found the decline in patient-experience scores occurred mainly in hospitals acquired by hospitals that already had a poor patient-experience score—a finding that suggests acquisitions facilitate the spread of low quality care but not of high quality care.

The researchers caution that isolated, individual mergers may have still yielded positive results—something that an aggregate analysis is not powered to capture. And the researchers could only examine measurable aspects of quality. The trend in hospital performance on these standard measures, however, appears to point to a net effect of overall decline, the team said.

“Since our study estimated the average effects of mergers, we can’t rule out the possibility that some mergers are good for patient care,” said first author Nancy Beaulieu, research associate in health care policy at HMS. “But this evidence should give us pause when considering arguments for hospitals mergers.”

The work was supported by the Agency for Healthcare Research and Quality (grant no. U19HS024072).

Co-investigators included Bruce Landon and Jesse Dalton from HMS, Ifedayo Kuye, from the University of California, San Francisco, and Leemore Dafny from Harvard Business School and the National Bureau of Economic Research.

Source: https://hms.harvard.edu/news/hospital-mergers-quality-care

Public Benefit Corporations (PBC)

Public benefit corporations (versus Benefit Corporate status, which is more of a pledge) are separate legal entities which exist as a hybrid, for-profit/nonprofit company but is mandated to

- Pursue a general or specific public benefit

- Consider the non-financial interests of its shareholders and other STAKEHOLDERS when making decision

- report how well it is achieving its overall public benefit objectives

- Have limited fiduciary responsibility to investors that remains IN SCOPE of public benefit goal

In essence, the public benefit corporations executives are mandated to run the company for the benefit of STAKEHOLDERS first, if those STAKEHOLDERS are the public beneficiary of the company’s goals. This in essence moves the needle away from the traditional C-Corp overvaluing the needs of shareholders and brings back the mission of the company and in the case of healthcare, the needs of its stakeholders, the consumers of healthcare.

PBCs are legal entities recognized by states rather than by the federal government. So far, in 2020 about 37 states allow companies to incorporate as a PBC. Stipulations of the charter include semiannual reporting of the public benefits bestowed by the company and how well it is achieving its public benefit mandate. There are about 3,000 US PBCs. Some companies have felt it was in their company mission and financial interest to change incorporation as a PBC.

Some well known PBCs include

- Ben and Jerry’s Ice Cream

- American Red Cross

- Susan B. Komen Foundation

- Allbirds (a shoe startup valued at $1.7 billion when made switch)

- Bombas (the sock company that donates extra socks when you buy a pair)

- Lemonade (a publicly traded insurance PBC that has beneficiaries select a nonprofit that the company will donate to)

Although the number of PBCs in the healthcare arena is increasing

- Not many PBCs are in the area of healthcare delivery

- Noone is quite sure what the economic model would look like for a healthcare delivery PBC

Some example of hospital PBC include NYC Health + Hospitals and Community First Medical Center in Chicago.

Benefits of moving a hospital to PBC Status

- PBCs are held legally accountable to a predefined public benefit. For hospitals this could be delivering cost-effective quality of care and affordable to a local citizenry or an economically disadvantaged population. PBCs must produce at least an annual report on the public benefits it has achieved contrasted against a third party standard. For example a hospital could include data of Medicaid related mortality risks, data neither the C-corp nor the nonprofit 501c would have to report on. Most nonprofits and charities report their taxes on a schedule H or Form 990, which only has to report the officer’s compensation as well as monies given to charitable organizations, or other 501 organizations. The nonprofit would show a balance of zero as the donated money for that year would be allocated out for various purposes. Hospitals, even as nonprofits, are not required to submit all this data. Right now in US the ACA just requires any hospital that receives government or ACA insurance payments to report certain outcome statistics. Although varying state by state, a PBC should have a “benefit officer” to make sure the mandate is being met. In some cases a PBC benefit officer could sue the board for putting shareholder interest over the public benefit mandate.

- A PBC can include community stakeholders in the articles of incorporation thus giving a voice to local community members. This would be especially beneficial for a hospital serving, say, a rural community.

- PBCs do have advantages of the for-profit companies as they are not limited to non-equity forms of investment. A PBC can raise money in the equity markets or take on debt and finance it. These financial instruments are unavailable to the non-profit. Yet one interesting aspect is that PBCs require a HIGHER voting threshold by shareholders than a traditional for profit company in the ability to change their public benefit or convert their PBC back to a for-profit.

Limitations of the PBC

- Little incentive financially for current and future hospitals to incorporate as a PBC. Herein lies a huge roadblock given the state of our reimbursement structure in this country. Although there may be an incentive with regard to hiring and retention of staff drawn to the organization’s social purpose. There have been, in the past, suggestions to allow hospitals that incorporate at PBC to receive some tax benefit, but this legislation has not gone through either at state or federal level. (put link to tax article).

- In order for there to be value to constituents (patients) there must be strong accountability measures. This will require the utmost in ethical behavior by a board and executives. We have witnessed, through M&A by large health groups, anticompetitive and near monopoly behavior.

- There are no federal guidelines but varying guidelines from state to state. There must be some federal recognition of the PBC status when it comes to healthcare, such as that the government is one of the biggest payers of US healthcare.

This is a great interview with ArcHealth, a PBC healthcare system.

Arc Health as a Public Benefit Company and Social Enterprise – What is the difference?

Mar 3, 2021 | Healthcare

Arc Health PBC is a public benefit corporation, a mission-driven for-profit company that utilizes a market-driven approach to achieving our short and long-term social goals. As a public benefit corporation, Arc Health is also a social enterprise working to further our mission of providing healthcare to rural, underserved, and indigenous communities through business practices that improve the recruitment and retention of quality healthcare providers.

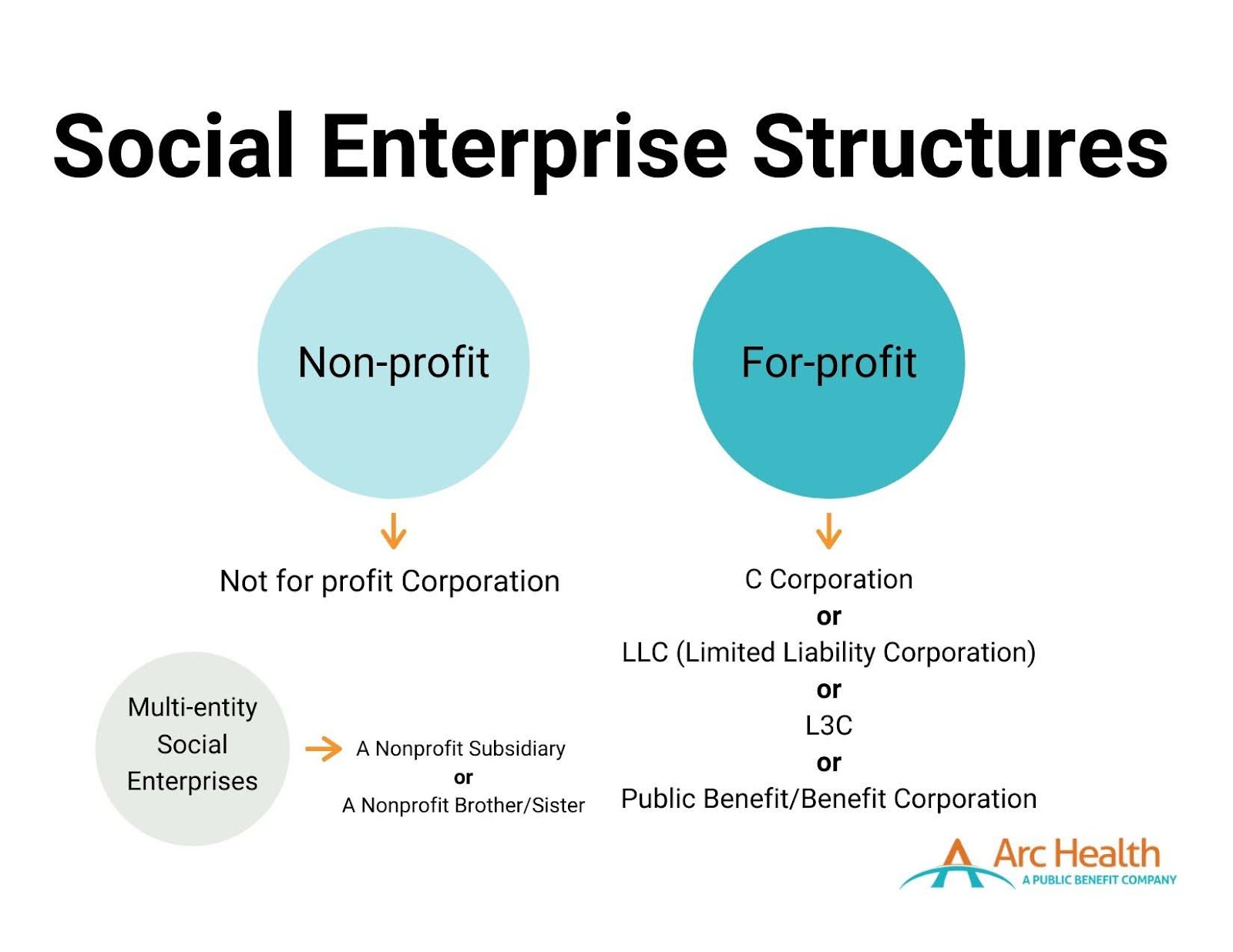

What is a Social Enterprise?

While there is no one exact definition, according to the Social Enterprise Alliance, a social enterprise is an “organization that addresses a basic unmet need or solves a social or environmental problem through a market-driven approach.” A social enterprise is not a distinct legal entity, but instead, an “ideological spectrum marrying commercial approaches with social good.” Social enterprises foster a dual-bottom-line – simultaneously seeking profits and social impact. Arc Health, like many social enterprises, seeks to be self–sustainable.

Two primary structures fall under the social enterprise umbrella: nonprofits and for-profit organizations. There are also related entities within both structures that could be considered social enterprises. Any of these listed structures can be regarded as a social enterprise depending on if and how involved they are with socially beneficial programs.

What is a Public Benefit Corporation?