Can the Public Benefit Company Structure Save US Healthcare?

Curator: Stephen J. Williams, Ph.D.

UPDATED 11/05/2023

Public Benefit Corporation structure in healthcare has actually been around since the 1970s in New Yourk State, when New York City’s new Health and Hospitals Corporation took over the city Department of Hospitals and today runs 11 hospitals and four long-term care facitlites in the city. The following link to an article describes however the problems occuring with Nassau and Westchester hosptial systems, which were converted to New York PBC status in the 1990s. As the article states the financial problems in 2004 which these hospitals encountered

do not stem from their unusual status as public benefit corporations, and might have been even worse off had they not converted

The New York Times article of 2004 “At 2 Hospitals, Fiscal Troubles in the Glare of Public View” highlight in fact the growing problem that all hospitals are encountering, especially on the fiscal side. But it does highlight how to better structure these entities and why full commitment to the PBC structure is necessary.

In 2003 New York State had a record closure of hospitals, and in 2004 Nassau and WestChester were having such fiscal problems it threatened the bond status of those counties. Despite the regular problems hospitals had, critics had said there were two major contributing factors to their woes

- the two agencies had not completed their transition from government operations to fully competitve hospitals

- as a PBC they bear a costly mission of serving the uninsured

As a PBC the structure allows one to shed cumbersome government rules, giving them the flexibility to conduct business like other hospitals.

In addition they are no longer dependent, in fact now forced, to forgo dependence on public funding and look for independent means of investment. With their semi-independence from government the agencies also are more insulted from political pressure.

However this seemed to be the problem. These agencies were still to dependent on their local government and there was still local political influence on their boards.

UPDATED 3/15/2023

According to Centers for Medicare and Medicare Services (CMS.gov) healthcare spending per capita has reached 17.7 percent of GDP with, according to CMS data:

From 1960 through 2013, health spending rose from $147 per person to $9,255 per person, an average annual increase of 8.1 percent.

the National Health Expenditure Accounts (NHEA) are the official estimates of total health care spending in the United States. Dating back to 1960, the NHEA measures annual U.S. expenditures for health care goods and services, public health activities, government administration, the net cost of health insurance, and investment related to health care. The data are presented by type of service, sources of funding, and type of sponsor.

U.S. health care spending grew 4.6 percent in 2019, reaching $3.8 trillion or $11,582 per person. As a share of the nation’s Gross Domestic Product, health spending accounted for 17.7 percent.

And as this spending grew (demand for health care services) associated costs also rose but as the statistical analyses shows there was little improvement in many health outcome metrics during the same time.

It appears that US healthcare may be on the precipice of a transformational shift, but what will this shift look like? The following post examines if the corporate structure of US healthcare needs to be changed and what role does a Public Benefit Company have in this much needed transformation.

Hippocratic Oath

I swear by Apollo the physician, and Asclepius, and Hygieia and Panacea and all the gods and goddesses as my witnesses, that, according to my ability and judgement, I will keep this Oath and this contract:

To hold him who taught me this art equally dear to me as my parents, to be a partner in life with him, and to fulfill his needs when required; to look upon his offspring as equals to my own siblings, and to teach them this art, if they shall wish to learn it, without fee or contract; and that by the set rules, lectures, and every other mode of instruction, I will impart a knowledge of the art to my own sons, and those of my teachers, and to students bound by this contract and having sworn this Oath to the law of medicine, but to no others.

I will use those dietary regimens which will benefit my patients according to my greatest ability and judgement, and I will do no harm or injustice to them.

I will not give a lethal drug to anyone if I am asked, nor will I advise such a plan; and similarly I will not give a woman a pessary to cause an abortion.

In purity and according to divine law will I carry out my life and my art.

I will not use the knife, even upon those suffering from stones, but I will leave this to those who are trained in this craft.

Into whatever homes I go, I will enter them for the benefit of the sick, avoiding any voluntary act of impropriety or corruption, including the seduction of women or men, whether they are free men or slaves.

Whatever I see or hear in the lives of my patients, whether in connection with my professional practice or not, which ought not to be spoken of outside, I will keep secret, as considering all such things to be private.

So long as I maintain this Oath faithfully and without corruption, may it be granted to me to partake of life fully and the practice of my art, gaining the respect of all men for all time. However, should I transgress this Oath and violate it, may the opposite be my fate.

Translated by Michael North, National Library of Medicine, 2002.

Much of the following information can be found on the Health Affairs Blog in a post entitled

Public Benefit Corporations: A Third Option For Health Care Delivery?

By Soleil Shah, Jimmy J. Qian, Amol S. Navathe, Nirav R. Shah

Limitations of For Profit and Non-Profit Hospitals

For profit represent ~ 25% of US hospitals and are owned and governed by shareholders, and can raise equity through stock and bond markets.

According to most annual reports, the CEOs incorrectly assume they are legally bound as fiduciaries to maximize shareholder value. This was a paradigm shift in priorities of companies which started around the mid 1980s, a phenomenon discussed below.

A by-product of this business goal, to maximize shareholder value, is that CEO pay and compensation is naturally tied to equity markets. A means for this is promoting cost efficiencies, even in the midst of financial hardships.

A clear example of the failure of this system can be seen during the 2020- current COVID19 pandemic in the US. According to the Medicare Payment Advisory Commission, four large US hospitals were able to decrease their operating expenses by $2.3 billion just in Q2 2020. This amounted to 65% of their revenue; in comparison three large NONPROFIT hospitals reduced their operating expense by an aggregate $13 million (only 1% of their revenue), evident that in lean times for-profit will resort to drastic cost cutting at expense of service, even in times of critical demands for healthcare.

Because of their tax structure and perceived fiduciary responsibilities, for-profit organizations (unlike non-profit and public benefit corporations) are not legally required to conduct community health need assessments, establish financial assistance policies, nor limit hospital charges for those eligible for financial assistance. In addition to the difference in tax liability, for-profit, unlike their non-profit counterparts, at least with hospitals, are not funded in part by state or local government. As we will see, a large part of operating revenue for non-profit university based hospitals is state and city funding.

Therefore risk for financial responsibility is usually assumed by the patient, and in worst case, by the marginalized patient populations on to the public sector.

Tax Structure Considerations of for-profit healthcare

Financials of major for-profit healthcare entities (2020 annual)

Non-profit Healthcare systems

Nonprofits represent about half of all hospitals in the US. Most of these exist as a university structure, so retain the benefits of being private health systems and retaining the funding and tax benefits attributed to most systems of higher education. And these nonprofits can be very profitable. After taking in consideration the state, local, and federal tax exemptions these nonprofits enjoy, as well as tax-free donations from contributors (including large personal trust funds), a nonprofit can accumulate a large amount of revenue after expenses. In fact 82 nonprofit hospitals had $33 billion of net asset increase year-over-year (20% increase) from 2016 to 2017. The caveat is that this revenue over expenses is usually spent on research or increased patient services (this may mean expanding the physical infrastructure of the hospital or disseminating internal grant money to clinical investigators, expanding the hospital/university research assets which could result in securing even larger amount of external funding from government sources.

And although this model may work well for intercity university/healthcare systems, it is usually a struggle for the rural nonprofit hospitals. In 2020, ten out of 17 rural hospitals that went under were nonprofits. And this is not just true in the tough pandemic year. Over the past two decades multitude of nonprofit rural hospitals had to sell and be taken over by larger for-profit entities.

Hospital consolidation has led to a worse patient experience and no real significant changes in readmission or mortality data. (The article below is how over 130 rural hospitals have closed since 2010, creating a medical emergency in rural US healthcare)

https://www.nationalgeographic.com/history/article/appalachian-hospitals-are-disappearing

And according to the article below it is only to get worse

The authors of the Health Affairs blog feel a major disadvantage of both the for-profit and non-profit healthcare systems is “that both face limited accountability with respect to anticompettive mergers and acquisitions.”

More hospital consolidation is expected post-pandemic

Aug 10, 2020

By Rich Daly, HFMA Senior Writer and Editor

News | Coronavirus

More hospital consolidation is expected post-pandemic

- Hospital deal volume is likely to accelerate due to the financial damage inflicted by the coronavirus pandemic.

- The anticipated increase in volume did not show up in the latest quarter, when deals were sharply down.

- The pandemic may have given hospitals leverage in coming policy fights over billing and the creation of “public option” health plans.

Hospital consolidation is likely to increase after the COVID-19 pandemic, say both critics and supporters of the merger-and-acquisition (M&A) trend.

The financial effects of the coronavirus pandemic are expected to drive more consolidation between and among hospitals and physician practices, a group of policy professionals told a recent Washington, D.C.-based web briefing sponsored by the Alliance for Health Policy.

“There is a real danger that this could lead to more consolidation, which if we’re not careful could lead to higher prices,” said Karyn Schwartz, a senior fellow at the Kaiser Family Foundation (KFF).

Schwartz cited a recent KFF analysis of available research that concluded “provider consolidation leads to higher health care prices for private insurance; this is true for both horizontal and vertical consolidation.”

Kenneth Kaufman, managing director and chair of Kaufman Hall, noted that crises tend to push financially struggling organizations “further behind.”

“I wouldn’t be surprised at all if that happens,” Kaufman said. “That will lead to further consolidation in the provider market.”

The initial rounds of federal assistance from the CARES Act, which were based first on Medicare revenue and then on net patient revenue, may fuel consolidation, said Mark Miller, PhD, executive vice president of healthcare for Arnold Ventures. That’s because the funding formulas favored organizations that already had higher revenues, he said, and provided less assistance to low-revenue organizations.

HHS has distributed $116.2 billion from the $175 billion in provider funding available through the CARES Act and the Paycheck Protection Program and Health Care Enhancement Act. The largest distributions used the two revenue formulas cited by Miller.

No surge in M&A yet

The expected burst in hospital M&A activity has yet to occur. Kaufman Hall identified 14 transactions in the second quarter of 2020, far fewer than in the same quarter in any of the four preceding years, when second-quarter transactions totaled between 19 and 31. The latest deals were not focused on small hospitals, with average seller revenue of more than $800 million — far larger than the previous second-quarter high of $409 million in 2018.

Six of the 14 announced transactions were divestitures by major for-profit health systems, including Community Health Systems, Quorum and HCA.

Kaufman Hall’s analysis of the recent deals identified another pandemic-related factor that may fuel hospital M&A: closer ties between hospitals. The analysis cited the example of Lifespan and Care New England, which had suspended merger talks in 2019. More recently, in a joint announcement, the CEOs of the two systems noted that because of the COVID-19 crisis, the two systems “have been working together in unprecedented ways” and “have agreed to enter into an exploration process to understand the pros and cons of what a formal continuation of this collaboration could look like in the future.”

The M&A outlook for rural hospitals

The pandemic has had less of a negative effect on the finances of rural hospitals that previously joined larger health systems, said Suzie Desai, senior director of not-for-profit healthcare for S&P Global.

A CEO of a health system with a large rural network told Kaufman the federal grants that the system received for its rural hospitals were much larger than the grants paid through the general provider fund.

“If that was true across the board, then the federal government recognized that many rural hospitals could be at risk of not being able to make payroll; actually running out of money,” Kaufman said. “And they seem to have bent over backwards to make sure that didn’t happen.”

Other CARES Act funding distributed to providers included:

- $12.8 billion for 959 safety net hospitals

- $11 billion to almost 4,000 rural healthcare providers and hospitals in urban areas that have certain special rural designations in Medicare

Telehealth has helped rural hospitals but has not been sufficient to address the financial losses inflicted by the pandemic, Desai said.

Other coming trends include a sharper cost focus

Desai expects an increasing focus “over the next couple years” on hospital costs because of the rising share of revenue received from Medicare and Medicaid. She expects increased efforts to use technology and data to lower costs.

Billy Wynne, JD, chairman of Wynne Health Group, expects telehealth restrictions to remain relaxed after the pandemic.

Also, the perceptions of the public and politicians about the financial health of hospitals are likely to give those organizations leverage in coming policy fights over changes such as banning surprise billing and creating so-called public-option health plans, Wynne said. As an example, he cited the Colorado legislature’s suspension of the launch of a public option “in part because of sensitivities around hospital finances in the COVID pandemic.”

“Once the dust settles, it’ll be interesting to see if their leverage has increased or decreased due to what we’ve been through,” Wynne said.

About the Author

Rich Daly, HFMA Senior Writer and Editor,

is based in the Washington, D.C., office. Follow Rich on Twitter: @rdalyhealthcare

Source: https://www.hfma.org/topics/news/2020/08/more-hospital-consolidation-is-expected-post-pandemic.html

From Harvard Medical School

Hospital Mergers and Quality of Care

A new study looks at the quality of care at hospitals acquired in a recent wave of consolidations

By JAKE MILLER January 16, 2020 Research

Image: NirutiStock / iStock / Getty Images Plus

The quality of care at hospitals acquired during a recent wave of consolidations has gotten worse or stayed the same, according to a study led by Harvard Medical School scientists published Jan. 2 in NEJM.

The findings deal a blow to the often-cited arguments that hospital consolidation would improve care. A flurry of earlier studies showed that mergers increase prices. Now after analyzing patient outcomes after hundreds of hospital mergers, the new research also dashes the hopes that this more expensive care might be of higher quality.

Get more HMS news here

“Our findings call into question claims that hospital mergers are good for patients—and beg the question of what we are getting from higher hospital prices,” said study senior author J. Michael McWilliams, the Warren Alpert Foundation Professor of Health Care Policy in the Blavatnik Institute at HMS and an HMS professor of medicine and a practicing general internist at Brigham and Women’s Hospital.

McWilliams noted that rising hospital prices have been one of the leading drivers of unsustainable growth in U.S. health spending.

To examine the impact of hospital mergers on quality of care, researchers from HMS and Harvard Business School examined patient outcomes from nearly 250 hospital mergers that took place between 2009 and 2013. Using data collected by the Centers for Medicare and Medicaid Services, they analyzed variables such as 30-day readmission and mortality rates among patients discharged from a hospital, as well as clinical measures such as timely antibiotic treatment of patients with bacterial pneumonia. The researchers also factored in patient experiences, such as whether those who received care at a given hospital would recommend it to others. For their analysis, the team compared trends in these indicators between 246 hospitals acquired in merger transactions and unaffected hospitals.

The verdict? Consolidation did not improve hospital performance, and patient-experience scores deteriorated somewhat after the mergers.

The study was not designed to examine the reasons behind the worsening in patient experience. Weakening of competition due to hospital mergers could have contributed, the researchers said, but deeper exploration suggested other potential mechanisms. Notably, the analysis found the decline in patient-experience scores occurred mainly in hospitals acquired by hospitals that already had a poor patient-experience score—a finding that suggests acquisitions facilitate the spread of low quality care but not of high quality care.

The researchers caution that isolated, individual mergers may have still yielded positive results—something that an aggregate analysis is not powered to capture. And the researchers could only examine measurable aspects of quality. The trend in hospital performance on these standard measures, however, appears to point to a net effect of overall decline, the team said.

“Since our study estimated the average effects of mergers, we can’t rule out the possibility that some mergers are good for patient care,” said first author Nancy Beaulieu, research associate in health care policy at HMS. “But this evidence should give us pause when considering arguments for hospitals mergers.”

The work was supported by the Agency for Healthcare Research and Quality (grant no. U19HS024072).

Co-investigators included Bruce Landon and Jesse Dalton from HMS, Ifedayo Kuye, from the University of California, San Francisco, and Leemore Dafny from Harvard Business School and the National Bureau of Economic Research.

Source: https://hms.harvard.edu/news/hospital-mergers-quality-care

Public Benefit Corporations (PBC)

Public benefit corporations (versus Benefit Corporate status, which is more of a pledge) are separate legal entities which exist as a hybrid, for-profit/nonprofit company but is mandated to

- Pursue a general or specific public benefit

- Consider the non-financial interests of its shareholders and other STAKEHOLDERS when making decision

- report how well it is achieving its overall public benefit objectives

- Have limited fiduciary responsibility to investors that remains IN SCOPE of public benefit goal

In essence, the public benefit corporations executives are mandated to run the company for the benefit of STAKEHOLDERS first, if those STAKEHOLDERS are the public beneficiary of the company’s goals. This in essence moves the needle away from the traditional C-Corp overvaluing the needs of shareholders and brings back the mission of the company and in the case of healthcare, the needs of its stakeholders, the consumers of healthcare.

PBCs are legal entities recognized by states rather than by the federal government. So far, in 2020 about 37 states allow companies to incorporate as a PBC. Stipulations of the charter include semiannual reporting of the public benefits bestowed by the company and how well it is achieving its public benefit mandate. There are about 3,000 US PBCs. Some companies have felt it was in their company mission and financial interest to change incorporation as a PBC.

Some well known PBCs include

- Ben and Jerry’s Ice Cream

- American Red Cross

- Susan B. Komen Foundation

- Allbirds (a shoe startup valued at $1.7 billion when made switch)

- Bombas (the sock company that donates extra socks when you buy a pair)

- Lemonade (a publicly traded insurance PBC that has beneficiaries select a nonprofit that the company will donate to)

Although the number of PBCs in the healthcare arena is increasing

- Not many PBCs are in the area of healthcare delivery

- Noone is quite sure what the economic model would look like for a healthcare delivery PBC

Some example of hospital PBC include NYC Health + Hospitals and Community First Medical Center in Chicago.

Benefits of moving a hospital to PBC Status

- PBCs are held legally accountable to a predefined public benefit. For hospitals this could be delivering cost-effective quality of care and affordable to a local citizenry or an economically disadvantaged population. PBCs must produce at least an annual report on the public benefits it has achieved contrasted against a third party standard. For example a hospital could include data of Medicaid related mortality risks, data neither the C-corp nor the nonprofit 501c would have to report on. Most nonprofits and charities report their taxes on a schedule H or Form 990, which only has to report the officer’s compensation as well as monies given to charitable organizations, or other 501 organizations. The nonprofit would show a balance of zero as the donated money for that year would be allocated out for various purposes. Hospitals, even as nonprofits, are not required to submit all this data. Right now in US the ACA just requires any hospital that receives government or ACA insurance payments to report certain outcome statistics. Although varying state by state, a PBC should have a “benefit officer” to make sure the mandate is being met. In some cases a PBC benefit officer could sue the board for putting shareholder interest over the public benefit mandate.

- A PBC can include community stakeholders in the articles of incorporation thus giving a voice to local community members. This would be especially beneficial for a hospital serving, say, a rural community.

- PBCs do have advantages of the for-profit companies as they are not limited to non-equity forms of investment. A PBC can raise money in the equity markets or take on debt and finance it. These financial instruments are unavailable to the non-profit. Yet one interesting aspect is that PBCs require a HIGHER voting threshold by shareholders than a traditional for profit company in the ability to change their public benefit or convert their PBC back to a for-profit.

Limitations of the PBC

- Little incentive financially for current and future hospitals to incorporate as a PBC. Herein lies a huge roadblock given the state of our reimbursement structure in this country. Although there may be an incentive with regard to hiring and retention of staff drawn to the organization’s social purpose. There have been, in the past, suggestions to allow hospitals that incorporate at PBC to receive some tax benefit, but this legislation has not gone through either at state or federal level. (put link to tax article).

- In order for there to be value to constituents (patients) there must be strong accountability measures. This will require the utmost in ethical behavior by a board and executives. We have witnessed, through M&A by large health groups, anticompetitive and near monopoly behavior.

- There are no federal guidelines but varying guidelines from state to state. There must be some federal recognition of the PBC status when it comes to healthcare, such as that the government is one of the biggest payers of US healthcare.

This is a great interview with ArcHealth, a PBC healthcare system.

Arc Health as a Public Benefit Company and Social Enterprise – What is the difference?

Mar 3, 2021 | Healthcare

Arc Health PBC is a public benefit corporation, a mission-driven for-profit company that utilizes a market-driven approach to achieving our short and long-term social goals. As a public benefit corporation, Arc Health is also a social enterprise working to further our mission of providing healthcare to rural, underserved, and indigenous communities through business practices that improve the recruitment and retention of quality healthcare providers.

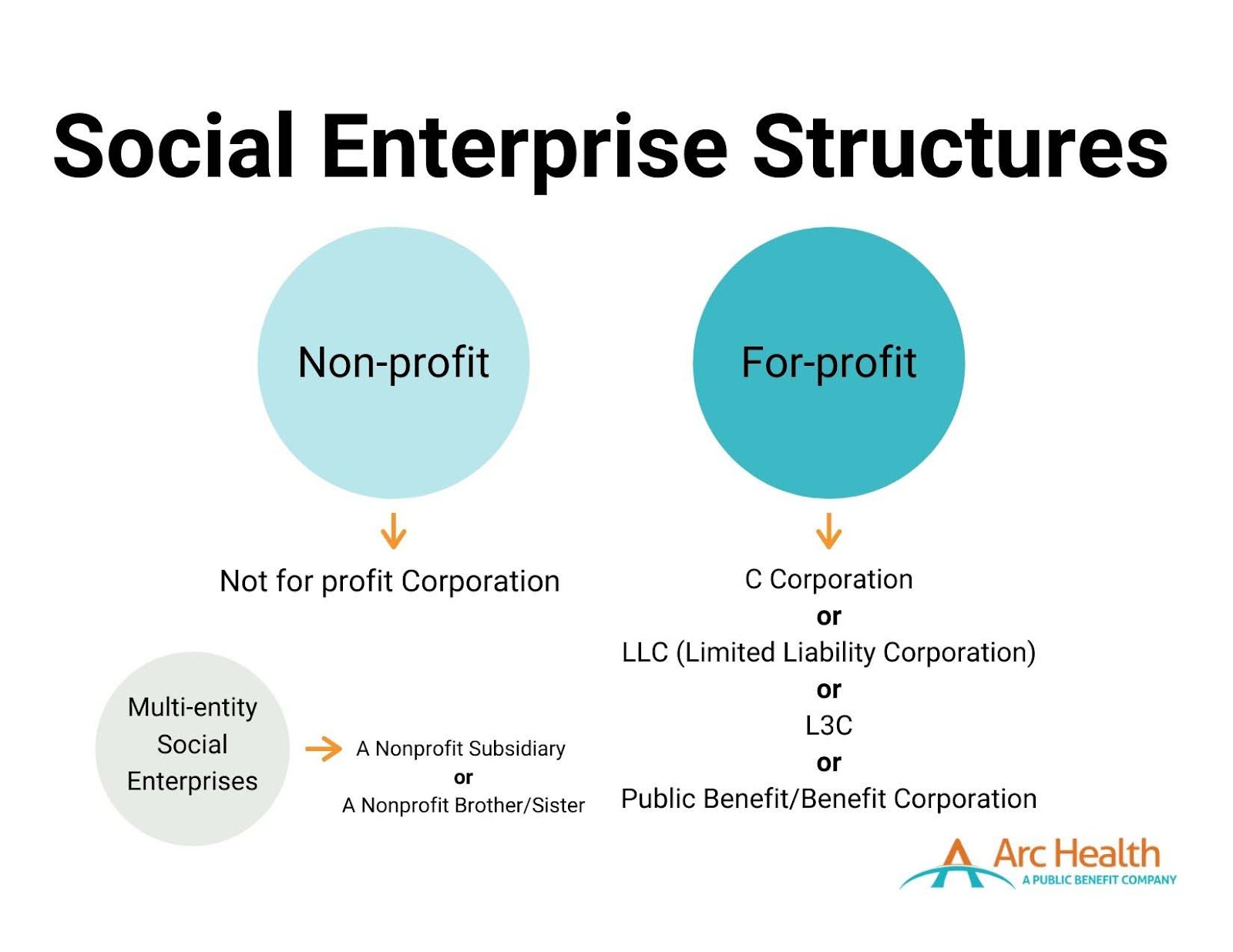

What is a Social Enterprise?

While there is no one exact definition, according to the Social Enterprise Alliance, a social enterprise is an “organization that addresses a basic unmet need or solves a social or environmental problem through a market-driven approach.” A social enterprise is not a distinct legal entity, but instead, an “ideological spectrum marrying commercial approaches with social good.” Social enterprises foster a dual-bottom-line – simultaneously seeking profits and social impact. Arc Health, like many social enterprises, seeks to be self–sustainable.

Two primary structures fall under the social enterprise umbrella: nonprofits and for-profit organizations. There are also related entities within both structures that could be considered social enterprises. Any of these listed structures can be regarded as a social enterprise depending on if and how involved they are with socially beneficial programs.

What is a Public Benefit Corporation?

Public Benefit Corporations (PBCs), also known as benefit corporations, are “for-profit companies that balance maximizing value to stakeholders with a legally binding commitment to a social or environmental mission.” PBCs operate as for-profit entities with no tax advantages or exemptions. Still, they must have a “purpose of creating general public benefit,” such as promoting the arts or science, preserving the environment, or providing benefits to underserved communities. PBCs must attain a higher degree of corporate purpose, expanded accountability, and expected transparency.

There are now over 3,000 registered PBCs, comprising approximately 0.1% of American businesses.

As a PBC, Arc Health expects to access capital through individual investors who seek financial returns, rather than through donations. Arc Health’s investors make investments with a clear understanding of the balance the company must strike between financial returns (I.e., profitability) and social purpose. Therefore, investors expect the company to be operationally profitable to ensure a financial return on their investments, while also making clear to all stakeholders and the public that generating social impact is the priority.

What is the difference between a Social Enterprise and PBC?

Social enterprises and PBCs emulate similar ideals that value the importance and need to invoke social change vis-a-vis working in a market-driven industry. Public benefit corporations fall under the social enterprise umbrella. An organization may choose to use a social enterprise model and incorporate itself as either a not-for-profit, C-Corp, PBC, or other corporate structure.

How did Arc Health Become a Public Benefit Corporation?

Arc Health was initially formed as a C-Corp. In 2019, Arc Health’s CEO and Co-Founder, Dave Shaffer, guided the conversion from a C-Corp to a PBC, incorporated in Delaware. Today, Arc Health follows guidelines and expectations for PBCs, including adhering to the State of Delaware’s requirements for PBCs.

Why is Arc Health a Social Enterprise and Public Benefit Corporation?

Arc Health believes it is essential to commit ourselves to our mission and demonstrate our dedication through our actions. We work to adhere to the core values of accountability, transparency, and purpose. As a registered public benefit company and a social enterprise, we execute our drive to achieve health equity in tangible and effective ways that the communities we work with, our stakeholders, and our providers expect of us.

90% of Americans say that companies must not only say a product or service is beneficial, but they also need to prove its benefit.

When we partner with health clinics and hospitals, we aim to provide services that enact lasting change. For example, we work with healthcare providers who desire to contribute both clinical and non-clinical skills. In 2020, Arc Health clinicians developed COVID-19 response protocols and educational materials about the vaccines. They participated in pain management working groups. They identified and followed up with kids in the community who were overdue for a well-child check. Arc Health providers should be driven by a desire to develop a long-term relationship with a healthcare service provider and participate in its successes and challenges.

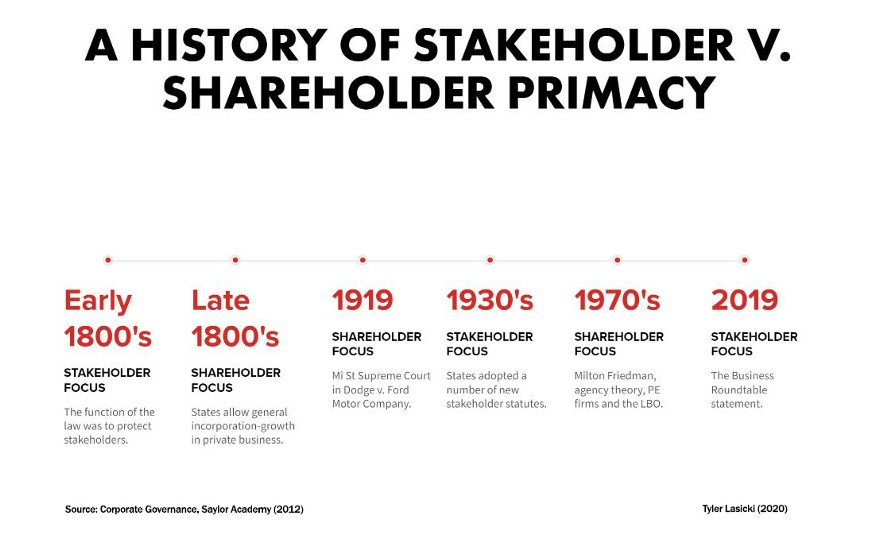

Paradigm Shift in the 1980’s: Companies Start to Emphasize Shareholders Over Stakeholders

So earlier in this post we had mentioned about a shift in philosophy at the corporate boardroom that affected how comparate thought, value, and responsibility: Companies in the 1980s started to shift their focus and value only the needs of corporate ShAREHOLDERS at the expense of their traditional STAKEHOLDERS (customers, clients). Many movies and books have been written on this and debatable if deliberate or a by-product of M&A, hostile takeovers, and the stock market in general but the effect was that the consumer was relegated as having less value, even though marketing budgets are very high. The fiduciary responsibility of the executive was now defined in terms of satisfying shareholders, who were now big huge and powerful brokerage houses, private equity, and hedge funds. A good explanation by Medium.com Tyler Lasicki is given below.

From the Medium.com

Source: https://medium.com/swlh/the-shareholder-v-stakeholder-contrast-a-brief-history-c5a6cfcaa111

The Shareholder V. Stakeholder Contrast, a Brief History

Follow

May 26, 2020 · 14 min read

Introduction

In a famous 1970 New York Times Article, Milton Friedman postulated that the CEO, as an employee of the shareholder, must strive to provide the highest possible return for all shareholders. Since that article, the United States has embraced this idea as the fundamental philosophy supporting the ultimate purpose of businesses — The Shareholders Come First.

In August of 2019, the Business Roundtable, a group made up of the most influential U.S CEOs, published a letter shifting their stance on the purpose of a corporation. Regardless of whether this piece of paper will actually result in any systematic changes has yet to be seen, however this newly stated purpose of business is a dramatic shift from the position Milton Friedman took in 1970. According to the statement, these corporations will no longer prioritize maximizing profits for shareholders, but instead turn their focus to benefiting all stakeholders — including citizens, customers, suppliers, employees, on par with shareholders.

Now the social responsibility of a company and the CEO was to maxiimize the profits even at the expense of any previous social responsibility they once had.

Small sample of the 181 Signatures attached to the Business Roundtable’s letter

What has happened over the past 50 years that has led to such a fundamental change in ideology? What has happened to make the CEO’s of America’s largest corporations suddenly change their stance on such a foundational principle of what it means to be an American business?

Since diving into this subject, I have come to find that the “American fundamental principle” of putting shareholders first is one that is actually not all that fundamental. In fact, for a large portion of our nation’s history this ideology was actually seen as the unpopular position.

Key ideological shifts in U.S. history

This post dives into a brief history of these two contrasting ideological viewpoints in an attempt to contextualize the forces behind both sides — specifically, the most recent shift (1970–2019). This basic idea of what is most important; the stakeholder or the shareholder, is the underlying reason as to why many things are the way they are today. A corporation’s priority of shareholder or stakeholder ultimately impacts employee salaries, benefits, quality of life within communities, environmental conditions, even the access to education children can receive. It affects our lives in a breadth and depth of ways and now that corporations may be changing positions (yet again) to focus on a model that prioritizes the stakeholder, it is important to understand why.

Looking forward, if stakeholder priority ends up being the popular position among American businesses, how long will it last for? What could lead to its downfall? And what will managers do to ensure a long term stakeholder-friendly business model?

It is clear to me the reasons that have led to these shifts in ideology are rather nuanced, however I want to highlight a few trends that have had a major impact on businesses changing their priorities while also providing context as to why things have shifted.

The Ascendancy of Shareholder Value

Following the 1929 stock market crash and the Great Depression, stakeholder primacy became the popular perspective within corporate America. Stakeholder primacy is the idea that corporations are to consider a wider group of interested parties (not just shareholders) whose positions need to be taken into consideration by corporate governance. According to this point of view, rather than solely being an agent for shareholders, management’s responsibilities were to be dispersed among all of its constituencies, even if it meant a reduction in shareholder value. This ideology lasted as the dominant position for roughly 40 years, in part due to public opinion and strong views on corporate responsibility, but also through state adoption of stakeholder laws.

By the mid-1970s, falling corporate profitability and stagnant share prices had been the norm for a decade. This poor economic performance influenced a growing concern in the U.S. regarding the perceived divergence between manager and shareholder interest. Many held the position that profits and share prices were suffering as a result of corporation’s increased attention on stakeholder groups.

This noticeable divergence in interests sparked many academics to focus their research on corporate management’s motivations in decision making regarding their allocation of resources. This branch of research would later be known as agency theory, which focused on the relationship between principals (shareholders) and their agents (management). Research at the time outlined how over the previous decades corporate management had pursued strategies that were not likely to optimize resources from a shareholder’s perspective. These findings were part of a seismic shift of corporate philosophy, changing priority from the stakeholders of a business to the shareholders.

By 1982, the U.S. economy started to recover from a prolonged period of high inflation and low economic growth. This recovery acted as a catalyst for change in many industries, leaving many corporate management teams to struggle in response to these changes. Their business performance suffered as a result. These distressed businesses became targets for a group of new investors…private equity firms.

Now the paradigm shift had its biggest backer…. private equity! And private equity care about ONE thing….. THEIR OWN SHARE VALUE and subsequently meaning corporate profit, which became the most important directive for the CEO.

So it is all hopeless now? Can there be a shift back to the good ‘ol days?

Well some changes are taking place at top corporate levels which may help the stakeholders to have a voice at the table, as the following IRMagazine article states.

And once again this is being led by the Business Roundtable, the same Business Roundtable that proposed the shift back in the 1970s.

Andrew Holt

REPORTER

Shift from shareholder value to stakeholder-focused model for top US firms

AUG 23, 2019

Business Roundtable reveals corporations to drop idea they function to serve shareholders only

Source: https://www.irmagazine.com/esg/shift-shareholder-value-stakeholder-focused-model-top-us-firms

Andrew Holt

REPORTER

n a major corporate shift, shareholder value is no longer the main objective of the US’ top company CEOs, according to the Business Roundtable, which instead emphasizes the ‘purpose of a corporation’ and a stakeholder-focused model.

The influential body – a group of chief executive officers from major US corporations – has stressed the idea of a corporation dropping the age-old notion that corporations function first and foremost to serve their shareholders and maximize profits.

Rather, the focus should be on investing in employees, delivering value to customers, dealing ethically with suppliers and supporting outside communities as the vanguard of American business, according to a Business Roundtable statement.

‘While each of our individual companies serves its own corporate purpose, we share a fundamental commitment to all of our stakeholders,’ reads the statement, signed by 181 CEOs. ‘We commit to deliver value to all of them, for the future success of our companies, our communities and our country.’

Gary LaBranche, president and CEO of NIRI, tells IR Magazine that this is part of a wider trend: ‘The redefinition of purpose from shareholder-focused to stakeholder-focused is not new to NIRI members. For example, a 2014 IR Update article by the late Professor Lynn Stout urges a more inclusive way of thinking about corporate purpose.’

NIRI has also addressed this concept at many venues, including the senior roundtable annual meeting and the NIRI Annual Conference, adds LaBranche. This trend was further seen in the NIRI policy statement on ESG disclosure, released in January this year.

Analyzing the meaning of this change in more detail, LaBranche adds: ‘The statement is a revolutionary break with the Business Roundtable’s previous position that the purpose of the corporation is to create value for shareholders, which was a long-held position championed by Milton Friedman.

‘The challenge is that Friedman’s thought leadership helped to inspire the legal and regulatory regime that places wealth creation for shareholders as the ‘prime directive’ for corporate executives.

‘Thus, commentators like Mike Allen of Axios are quick to point out that some shareholders may actually use the new statement to accuse CEOs of worrying about things beyond increasing the value of their shares, which, Allen reminds us, is the CEOs’ fiduciary responsibility.

‘So while the new Business Roundtable statement reflects a much-needed rebalancing and modernization that speaks to the comprehensive responsibilities of corporate citizens, we can expect that some shareholders will push back on this more inclusive view of who should benefit from corporate efforts and the capital that makes it happen. The new statement may not mark the dawn of a new day, but it perhaps signals the twilight of the Friedman era.’

In a similarly reflective way, Jamie Dimon, chairman and CEO of JPMorgan Chase & Co and chairman of the Business Roundtable, says: ‘The American dream is alive, but fraying. Major employers are investing in their workers and communities because they know it is the only way to be successful over the long term. These modernized principles reflect the business community’s unwavering commitment to continue to push for an economy that serves all Americans.’

Note: Mr Dimon has been very vocal for many years on corporate social responsibility, especially since the financial troubles of 2009.

Impact of New Regulatory Trends in M&A Deals

The following podcast from Pricewaterhouse Cooper Health Research Institute (called Next in Health) discusses some of the trends in healthcare M&A and is a great listen. However from 6:30 on the podcast discusses a new trend which is occuring in the healthcare company boardroom, which is this new focus on integrating companies that have proven ESG (or environmental, social, governance) functions within their organzations. As stated, doing an M&A deal with a company with strong ESG is looked favorably among regulators now.

Please click on the following link to hear a Google Podcast Next in Health episode

UPDATED 3/15/2023

Should There Be More Public Benefit Corporations in Health Care?

In a post by Heather Landi in Fierce Healthcare entitled

Health tech unicorn Aledade recently announced that it made the strategic decision to become a public benefit corporation (PBC).

The company joins just a handful of others in healthcare that are structured this way.

So what exactly is a PBC, and why does it matter?

PBCs are a type of for-profit corporate entity that has also adopted a public benefit purpose and is currently authorized by 35 states and the District of Columbia. A PBC must consider the nonfinancial interests of its shareholders and other stakeholders when making decisions. As a public benefit corporation, companies have to weigh their social/environmental objectives alongside maximizing value for shareholders.

While PBC and B Corp. are often used interchangeably, they are not the same. A B Corp. is a certification provided to eligible companies by the nonprofit, B Lab. A PBC is an actual legal entity that bakes into its certificate of incorporation a “public benefit,” according to Rubicon Law Group.

“I don’t think that there is a trade-off between either you do things that are good for society or you make profits in your business.” —Farzad Mostashari, M.D.

PBCs also are required to provide a report to shareholders every two years that detail how well the company is achieving its overall public benefit objectives. In some states, the report must be assessed against a third-party standard and be made publicly available. Delaware PBCs are not required to report publicly or against a third-party standard.

Aledade launched in 2014 and uses data analytics to help independent doctors’ offices transition to value-based care models. The company currently partners with more than 1,000 independent primary care practices comprising over 11,000 physicians and has nearly 150 contracts covering more than 1.7 million patients and $17 billion in total healthcare spending. Last June, the company raised $123 million in a series E round, boosting its valuation to $3.1 billion.

In a blog post, Aledade CEO and co-founder Farzad Mostashari, M.D., explained the company’s reasoning behind the move and said the corporate structure of a PBC is “well suited to mission-oriented companies where alignment with stakeholders is a key driver of the business model.”

“Aledade’s public benefit purpose means that we must weigh the interests of our primary care practice partners, their patients, our employees, and those who bear the burden of rising health care costs, alongside those of our shareholders, when we make decisions,” Mostashari said in an interview. This duty extends to all significant board decisions, including decisions on whether to go public, to make acquisitions or to sell the company, he noted.

The PBC structure helps create alignment among stakeholders and build trust, he said. “I don’t think that there is a trade-off between either you do things that are good for society or you make profits in your business. That might be true for fee-for-service businesses. It’s not true for Aledade,” he said.

He added, “For businesses that are built on trust and alignment, not considering stakeholder benefits gets you neither social good nor profits. If you’re in a business like our business where it’s actually really important that everybody have faith and belief that you are doing what’s best for patients, that you are actually in it for the long-term for practices, that’s what makes us successful as a business.”

Mark Cuban Cost Plus Drugs, which launched in January 2022 to offer low-cost rivals to overpriced generic drugs, also is structured as a public benefit corporation. The company’s founder and CEO Alexander Oshmyansky started the company in 2015 as a nonprofit, according to a feature story in D Magazine. Through Y Combinator, investors told Oshmyansky that the nonprofit model wouldn’t be able to raise the needed funds. He then reworked the business model to a PBC and launched Osh’s Affordable Pharmaceuticals in 2018.

Some other companies that are biotech drug development companies that operate under the PBC model include

rural healthcare startup Homeward Health,

Perlara, the first biotech PBC,

Rarebase, also a biotech company,

Sage Health At-Home,

Savvy Cooperative, which is described as “the first and only patient-owned public benefit co-op,”

Medicaid-focused company Waymark and

Trial Library, a cancer precision medicine company.

The pros and cons

Even a traditional for-profit C corporation can work toward a public mission without becoming a PBC. But, in an industry like healthcare, too often the duty to maximize financial returns for shareholders or investors can be in conflict with what is best for patients, executives say.

“With a startup, it might limit the ability to sell their business to a larger company in the future because there might be some limitations on what the larger company could do with the organization.”—Jodi Daniel, a partner in Crowell & Moring’s Health Care Group

According to some healthcare experts, PBCs offer a promising alternative as a business model for healthcare companies by providing a “North Star” by which a company can navigate critical business decisions.

“I think it really helps to drive accountability,” Huang, Osmind’s chief executive, said. “I think that’s important, especially in healthcare where it’s easy sometimes to get misaligned with all the different stakeholders that are involved in the industry. We wanted to make sure we had something to be accountable to. Second, it’s ingrained in the culture. The third element of why it was so helpful for us from the beginning is just on focus and alignment. I think we can be much more clear and transparent about what we’re focused on, our values, how we try to use that transparently to influence our decisions and how we can build a business that really ties all of that together.”

In a Health Affairs article, medical researchers at Stanford, including Jimmy Qian, a co-founder of Osmind, laid out the case for why PBCs may simultaneously improve individual patient outcomes and collective benefit without sacrificing institutions’ financial stability.

PBCs are held legally accountable to a predefined public benefit, which, for hospitals, could involve delivering high-quality, affordable care to local populations. PBCs are required to produce annual benefits reports that are assessed against a third-party standard. “These reports could be used by regulatory agencies such as the Centers for Medicare and Medicaid Services (CMS) or local health authorities to evaluate whether the PBC is making progress toward its stated mission and respond accordingly,” the researchers wrote.

But are there any trade-offs?

Having a public benefit obligation could potentially “tie the hands” of board members who can’t just focus on profits and must focus on those dual responsibilities, noted Jodi Daniel, a partner in Crowell & Moring’s Health Care Group.

“Companies that transition to being a public benefit corporation are intentionally trying to ensure that that the company’s mission doesn’t get diminished over time because it’s in their charter. So it helps [the mission] to endure. But there are pros and cons to that. It is somewhat binding the future board members and executives to follow that mission,” she said.

Daniel said she has spoken with several healthcare companies recently that are weighing the possibility of transitioning to a PBC. “Companies often don’t want to necessarily limit their options in their decision-making in the future. With a startup, it might limit the ability to sell their business to a larger company in the future because there might be some limitations on what the larger company could do with the organization,” she said in an interview.

By making decisions based on interests outside of financial ones, organizations may put themselves at a margin disadvantage as compared to pure for-profit players in the space, wrote Hospitalogy founder Blake Madden.

Faddis with Veeva said the company hasn’t seen any financial or performance trade-off as a result of operating as a PBC. He noted that the move has been good for recruiting, spurred more long-term conversations with customers and has been a source of new ideas.

“Prior to the conversion, you had employees who were thinking of new products or new functionality with the mindset of getting to be commercially successful,” Faddis said. “Now, you also have people thinking about it from the angle of, ‘Does it further one of our PBC purposes and then maybe it’s also going to be commercially successful?'”

Converting to a PBC also can be a tactic to build trust, Daniel noted, especially in healthcare, and that holds the potential to drive business.

One factor that isn’t clear is whether there is sufficient oversight to hold these companies accountable to their stated public mission. Who checks to make sure companies are making progress toward their objectives to improve healthcare?

Osmind publishes its benefit corporation report on its website to make it available to the public even though it is not required to do so. “I think that really highlights the accountability piece of you need to tell the world or at least tell your shareholders how you’re really trying to uphold your public benefit,” Huang said.